The page you were trying to view is not available for your role and region.

Financial markets are seemingly taking a glass half-full approach to recent developments in the Middle East, with global equities trading above where they were when the conflict broke out. Oil and gas markets have settled and stopped making new highs while bonds have stabilised and moved off their lowest levels to recoup some of their declines.

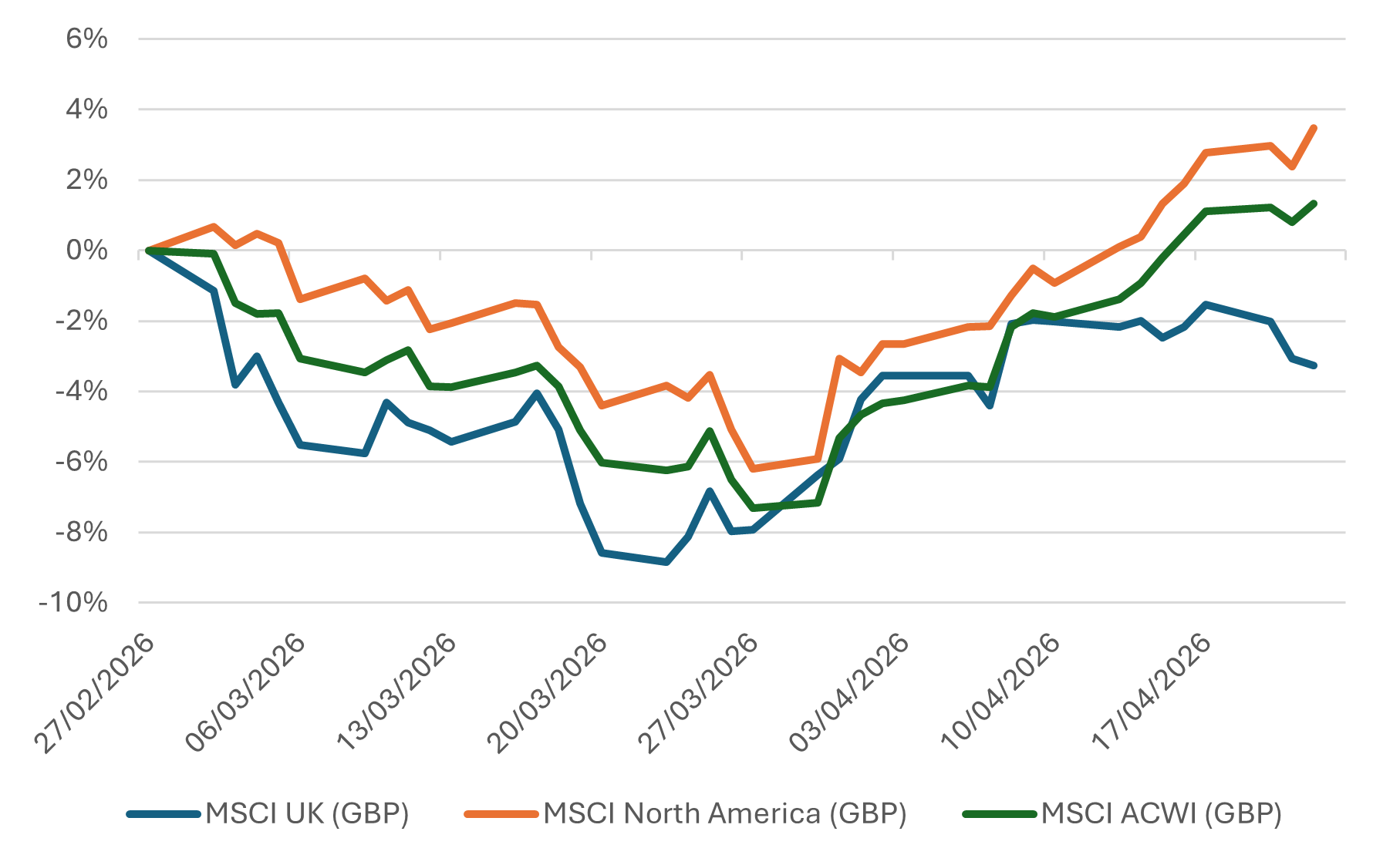

Chart 1: Stocks have recovered from the initial weakness after the Middle East conflict began, with the US performing best

Source: LSEG Datastream, Quilter Cheviot Limited, 23/4/2026. Past performance is not a reliable indicator of future results. The value of investments and the income from them can go down as well as up. You may not get back what you invest.

Two months have passed since the outbreak of war in the Middle East and although a lasting solution is yet to be found, markets are increasingly acting as if they believe that the Strait of Hormuz will see a return to pre-conflict shipping activity quite soon. There has been an on-off news flow of late, containing positive developments such as the agreement and subsequent extension of a two-week ceasefire brokered by Pakistan and negative events including the US navy seizure of an Iranian vessel.

Chart 2: US stocks have been one of the best performing markets since the conflict began

Source: LSEG Datastream, Quilter Cheviot Limited, 23/4/2026. Past performance is not a reliable indicator of future results. The value of investments and the income from them can go down as well as up. You may not get back what you invest.

Stocks have responded most positively in recent weeks, driven by US benchmarks reaching new all-time highs. During the first month or so of the conflict events in the Middle East appeared to be all consuming and front and centre of investors’ minds. More recently, other factors have come back to the fore, such as higher-than-expected earnings growth — Q1 US earnings are now forecast to be higher than before the war began and predicted to show double-digit growth for the sixth-consecutive quarter.

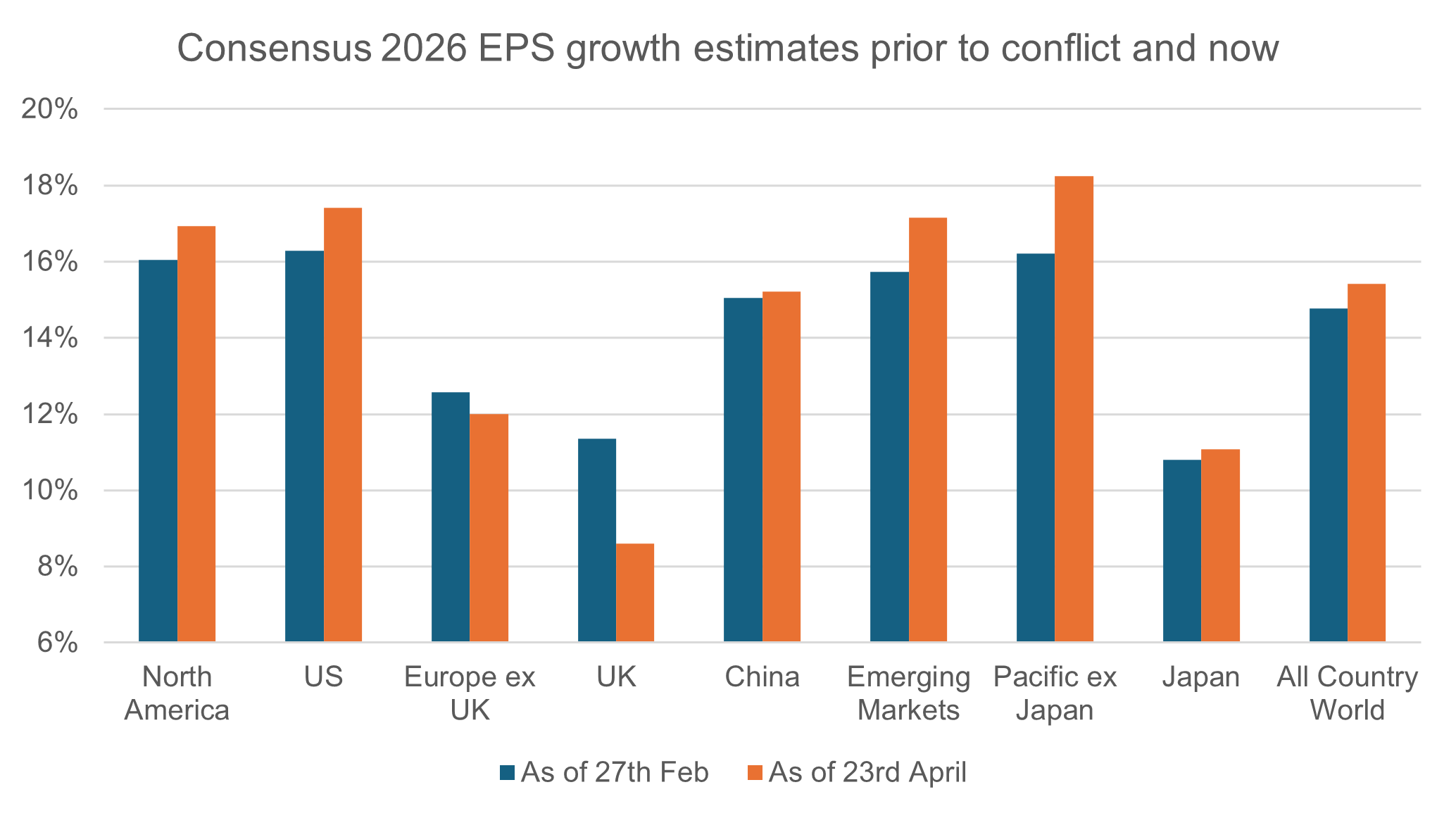

Chart 3: Global earnings growth forecasts have risen since the conflict began, but UK and European companies are now expected to grow more slowly

Source: LSEG Datastream, Quilter Cheviot Limited, 23/4/2026. Past performance is not a reliable indicator of future results. The value of investments and the income from them can go down as well as up. You may not get back what you invest.

There has been a notable divergence in earnings growth estimates across regions since the conflict began. Overall, the picture is more positive with the “all country world” estimate increasing due to higher estimates for the US, China, Japan, Emerging Markets and Pacific ex Japan countries. However, Europe ex UK has seen a mild downward revision to earnings growth expectations, while the UK has taken a substantial hit despite the apparent improved outlook for the sizable energy sector.

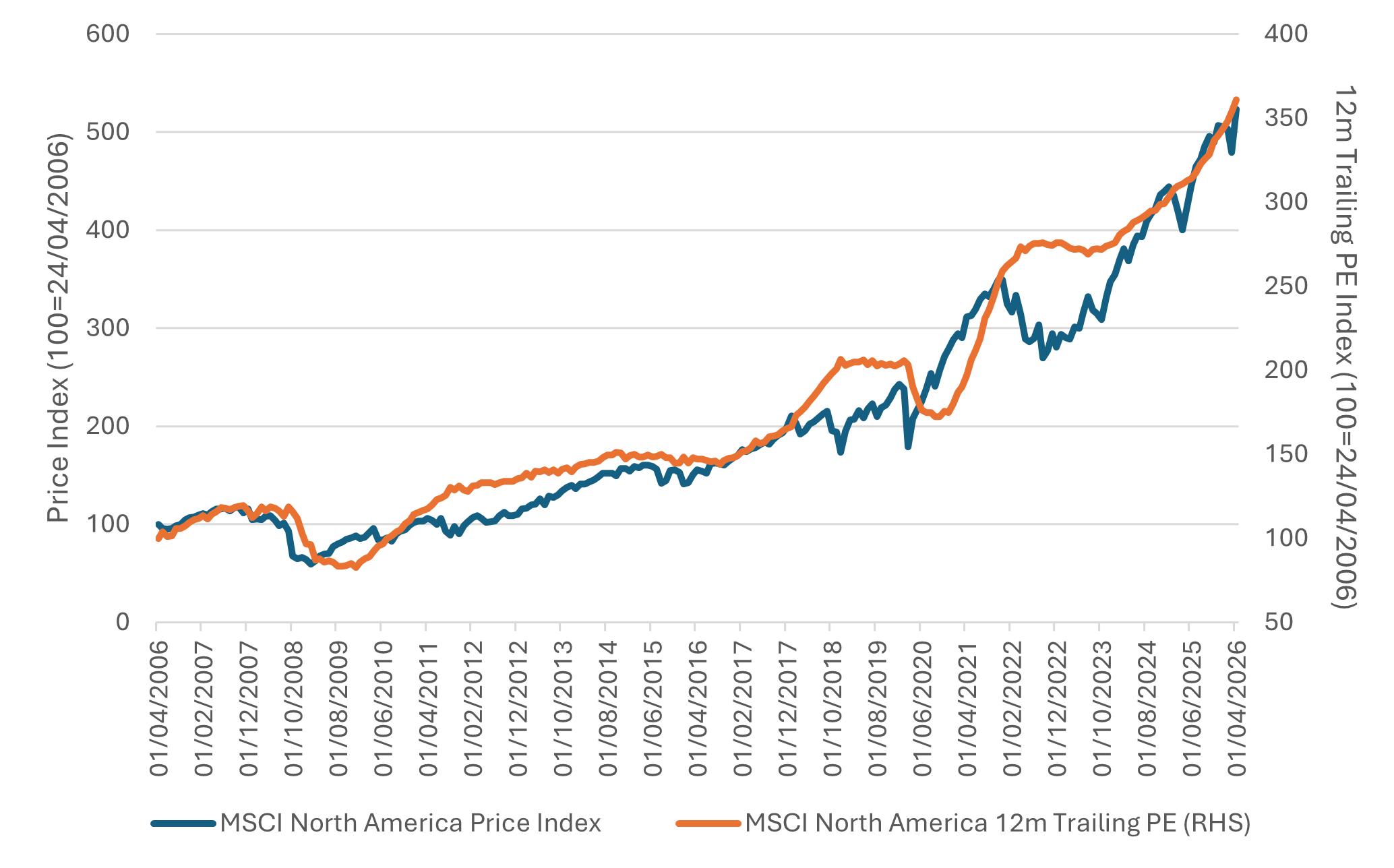

Chart 4: The rise of US stocks has been accompanied by rising earnings, providing reassurance that the gains are based on sound fundamental principles

Source: LSEG Datastream, Quilter Cheviot Limited, 23/4/2026. Past performance is not a reliable indicator of future results. The value of investments and the income from them can go down as well as up. You may not get back what you invest.

Those concerned about equity markets reaching new highs, should note that the performance for example of the MSCI North American index, is backed by trailing earnings also reaching new highs. This suggests the performance of markets in recent years is not illogical and has been backed by fundamentals.

However of course, the key questions now are, how high and for how long will oil and gas (and fertilizer etc) remain elevated, and therefore how much will the higher oil prices weigh on growth and inflation, and ultimately earnings, and therefore on share prices.

Corporate earnings can be viewed as a product of revenue growth, costs and operating leverage. In general terms, GDP growth can be seen as linked to revenue growth, while inflation can impact both revenue growth and costs. Company performance also determines costs as well as operating leverage. Therefore if GDP growth is significantly lower and/or inflation is significantly higher for a prolonged period then you would expect to see a negative impact on earnings growth. We are monitoring first quarter corporate updates closely for any signs that this is the case.

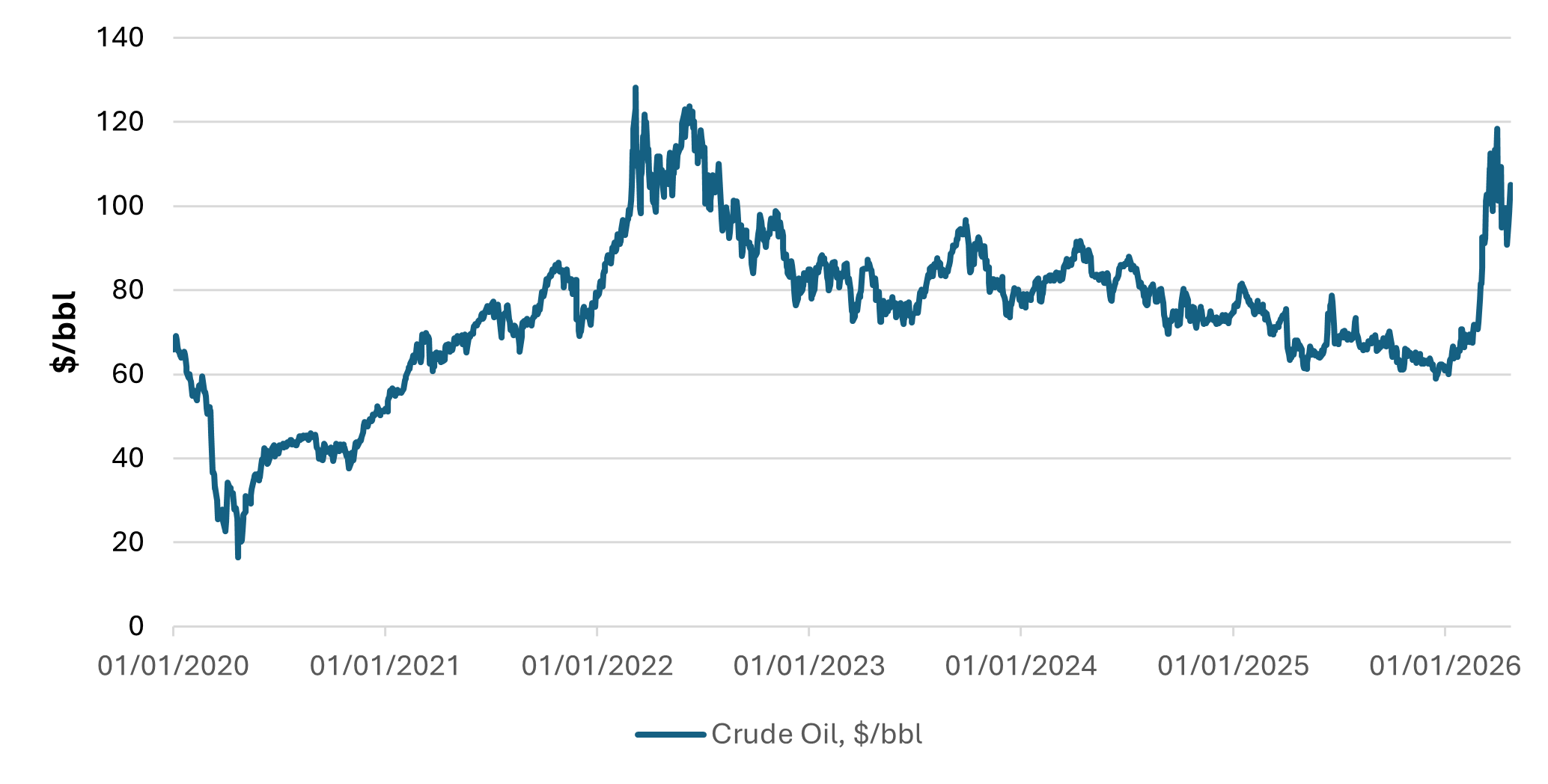

Oil higher but still below 2022 levels

If stocks have been the most optimistic in terms of a lasting positive resolution being found sooner rather than later, commodity markets have appeared the least hopeful. While Brent crude, an international benchmark for the oil price, has retreated from the highs set in early March it remains around the middle of its US$90-US$120 per barrel range since the conflict began.

Chart 5: Although the oil price has increased in the last two months, the level remains lower than that in 2022 when Russia invaded Ukraine

Source: LSEG Datastream, Quilter Cheviot Limited, 23/4/2026. Past performance is not a reliable indicator of future results. The value of investments and the income from them can go down as well as up. You may not get back what you invest.

Furthermore, benchmark prices may be underestimating the impact. A premium exists for delivering physical oil to a given location and these premia have risen sharply since the Strait of Hormuz shut. There have been reports of some shipments commanding a price as high as US$286 per barrel!

Around 20% of global oil and gas passed through the strait before the war and while it is technically open due to the current ceasefire, traffic remains considerably lower. Even if the strait were to open imminently, there will be lasting implications for energy markets for some time yet. We have approached two months of nearly 20m barrels per day of oil that normally transits the strait not flowing out into the world. Meanwhile somewhere in the range of 10m-15m barrels per day of oil production has been lost due to capacity shut downs either due to lack of storage or due to damage, which will come back online at varying speeds once the strait opens again.

Inventory drawdowns, including the IEA co-ordinated release of 400m barrels from strategic oil reserves held by member countries have softened the blow somewhat, while there has also been a reduction in demand due to higher prices.

The disruption has not been confined to the oil and gas sector, with a number of widely used commodities passing through the Strait of Hormuz before its effective closure. Around 20% of seaborne fertilizers, nearly half of all seaborne sulphur trade and approximately a third of seaborne methanol had passed through the strait.

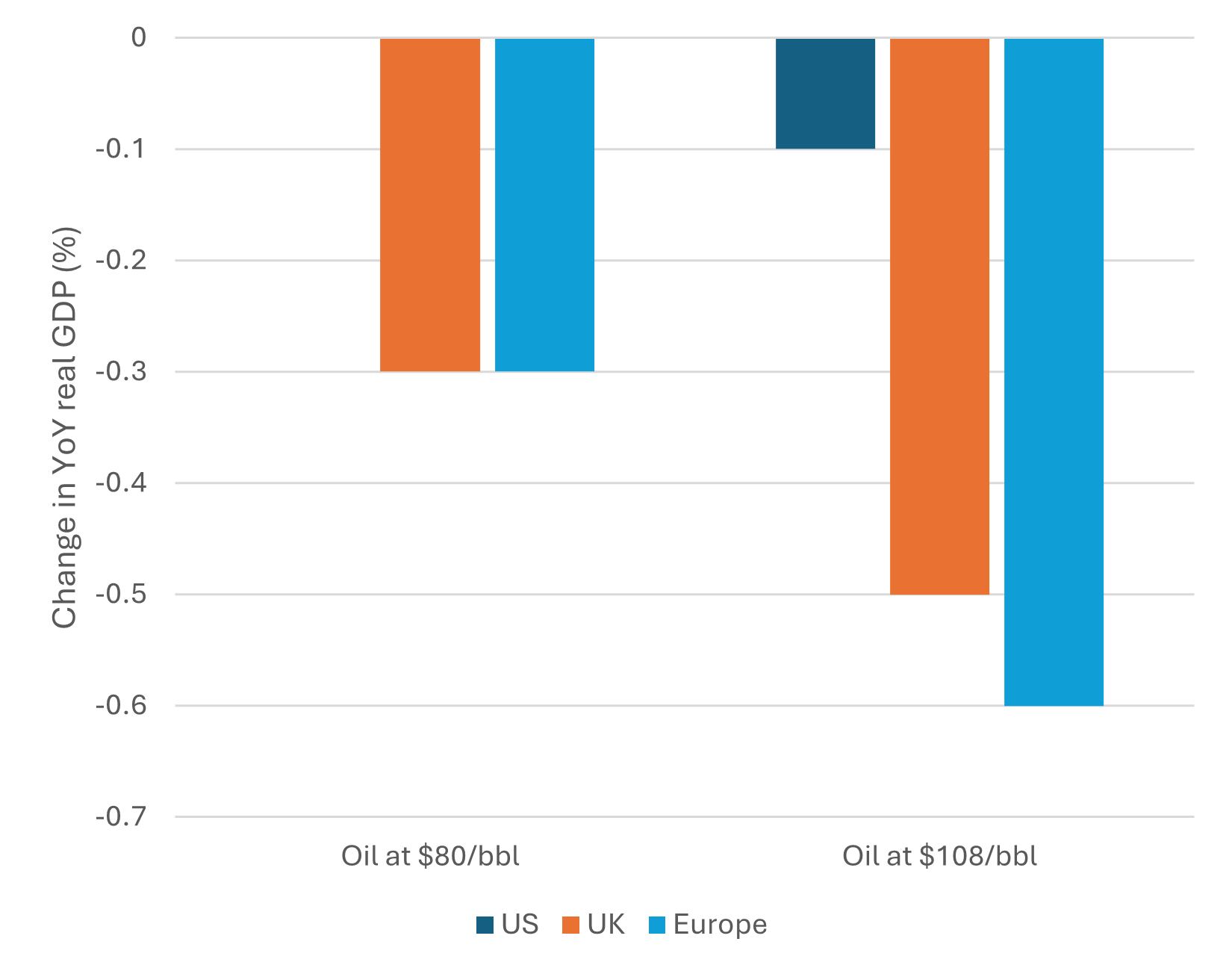

Some negative growth impact likely

The longer that oil prices remain elevated, the greater the negative impact on the global economy. To give some context, if the oil price averages US$80 per barrel for 3-6 months then, all else being equal (which it is not), the negative growth hit to UK and European GDP for 2026 would be limited to around 0.3% while the US would have no adverse impact (unlike the UK and EU, the US is not an energy importer and therefore its economy is far less sensitive to higher energy prices).

However, should oil remain around US$108 a barrel for a sustained period the impact on UK and European growth would be more meaningful, potentially taking 0.5% off UK GDP and 0.6% off European GDP. The US would only suffer a 0.1% hit. Since the war began the average price of oil has been lower than US$108 per barrel, but far closer to this level than to US$80 per barrel.

Chart 6: The negative impact on economic growth becomes more meaningful the higher the oil price

Source: Bloomberg economics, Quilter Cheviot Limited, 2/3/2026. Past performance is not a reliable indicator of future results. The value of investments and the income from them can go down as well as up. You may not get back what you invest.

The impact of the conflict so far on economic data has been somewhat muted, although some potential warning signs are beginning to flash. While activity has held up relatively well – recent composite purchasing managers’ index (PMI) output readings were steady for most major economies – this in part reflects a pull-forward of demand. Companies have rushed to build inventories in anticipation of future cost increases and disruption. The latest composite PMI data also showed a sharp rise in input prices, indicating a supply shock, most likely an indicator of higher output prices and lower demand to come.

As with earnings estimates, however, the data does appear to show some divergence between Europe and the UK on one hand, and the US on the other. US prices and activity appear to be less impacted, although consumer sentiment appears to be similarly hit on both sides of the Atlantic judging by recent consumer survey readings.

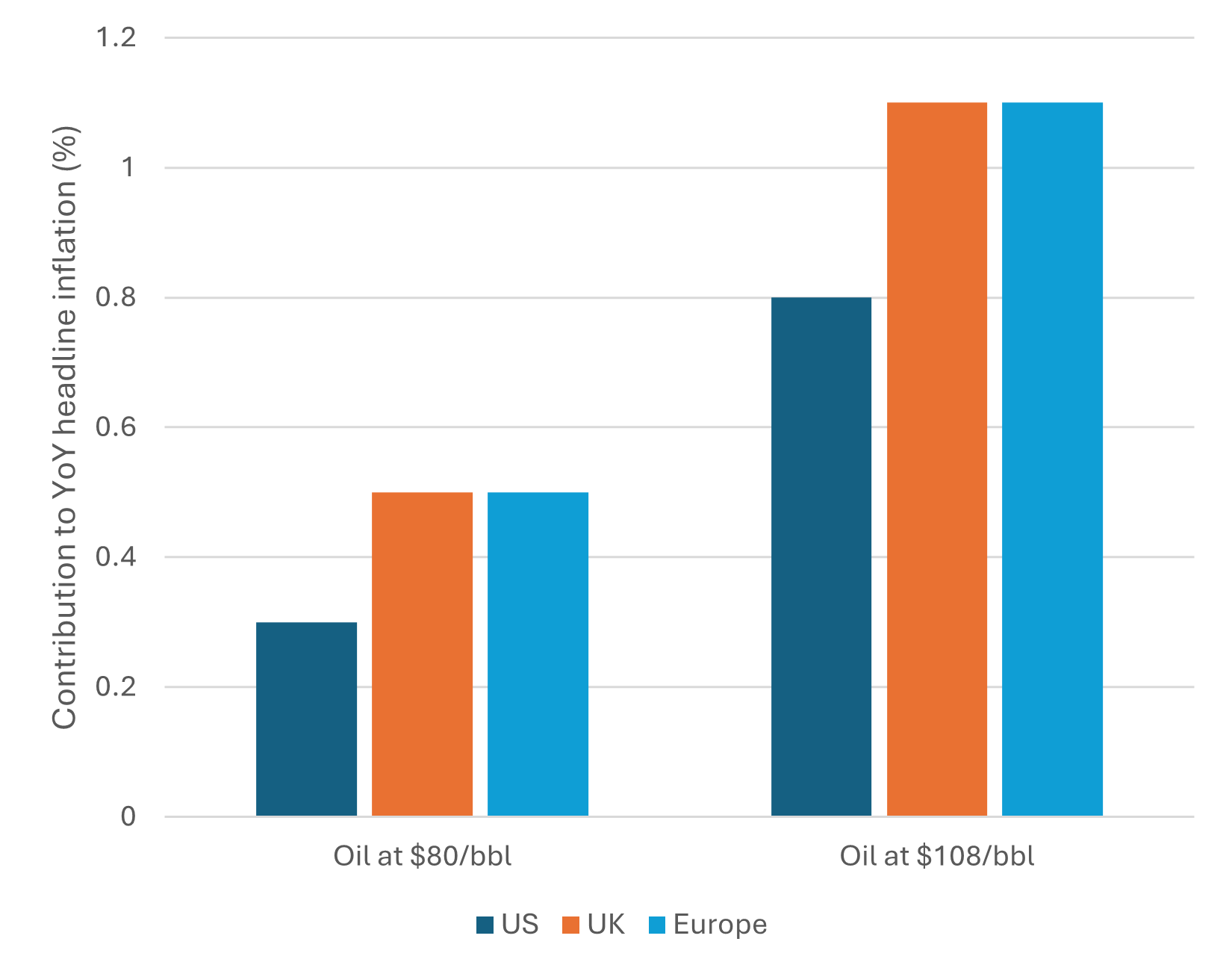

Inflation to rise but still some way short of 2022

Turning to inflation, which is seen as the bigger near-term risk, US$80 per barrel oil could lead to UK and European inflation rising to 0.5% and a 0.3% increase for US inflation. This is based on first-order impacts and doesn’t take into account second-order effects including potentially higher food prices. US$108 per barrel oil maintained for 3-6 months, may see a 1.1% rise in both UK and European inflation and a 0.8% increase for the US, a more meaningful impact.

We have started to see the first signs of this show up in economic data, with the UK consumer price index (CPI) rising to 3.3% y/y (year-on-year) in March, from 3.0% in February. The Eurozone equivalent rose to 2.5% in March from 1.9% in February and US CPI jumped to 3.3% from 2.4%. Not too much should be made of one monthly increase as these figures are notoriously volatile and subject to base level effects, but it is quite clear that we are already seeing higher price pressures feeding through.

Chart 7: Higher oil prices are expected to raise inflation, with the impact becoming more meaningful around the US$108 per barrel level or higher

Source: Bloomberg economics, Quilter Cheviot Limited, 2/3/2026. Past performance is not a reliable indicator of future results. The value of investments and the income from them can go down as well as up. You may not get back what you invest.

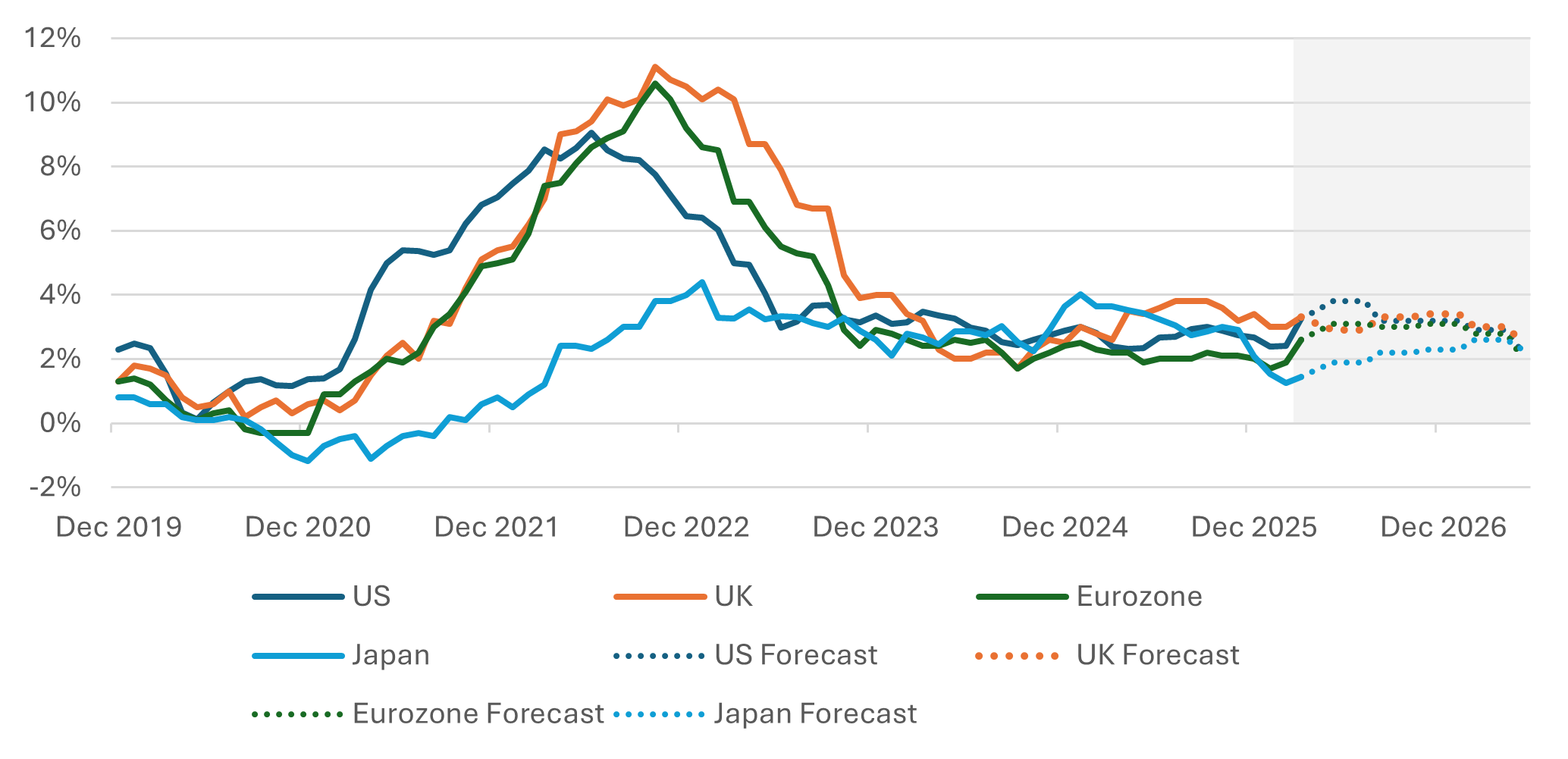

We have already seen the impact of the conflict in March’s inflation data and even if the war were to end tomorrow there will be lasting impacts. That said, the current environment is notably different to that in 2022 when inflation soared following the Russian invasion of Ukraine (which was compounded by a post-Covid 19 global demand increase). The latest UK CPI reading of 3.3% is well below the 6.2% seen in February 2022. Also, central bank base rates are at far more normal levels — BoE 3.75% currently vs 0.5% in February 2022; Fed 3.50%-3.75% currently vs 0.0%-0.25%; and ECB 2.0% vs 0.0%.

Chart 8: Headline CPI has risen but is not expected to rise much further, according to consensus forecasts among economists surveyed by Reuters

Source: LSEG Datastream, Quilter Cheviot Limited, 23/4/2026. Past performance is not a reliable indicator of future results. The value of investments and the income from them can go down as well as up. You may not get back what you invest.

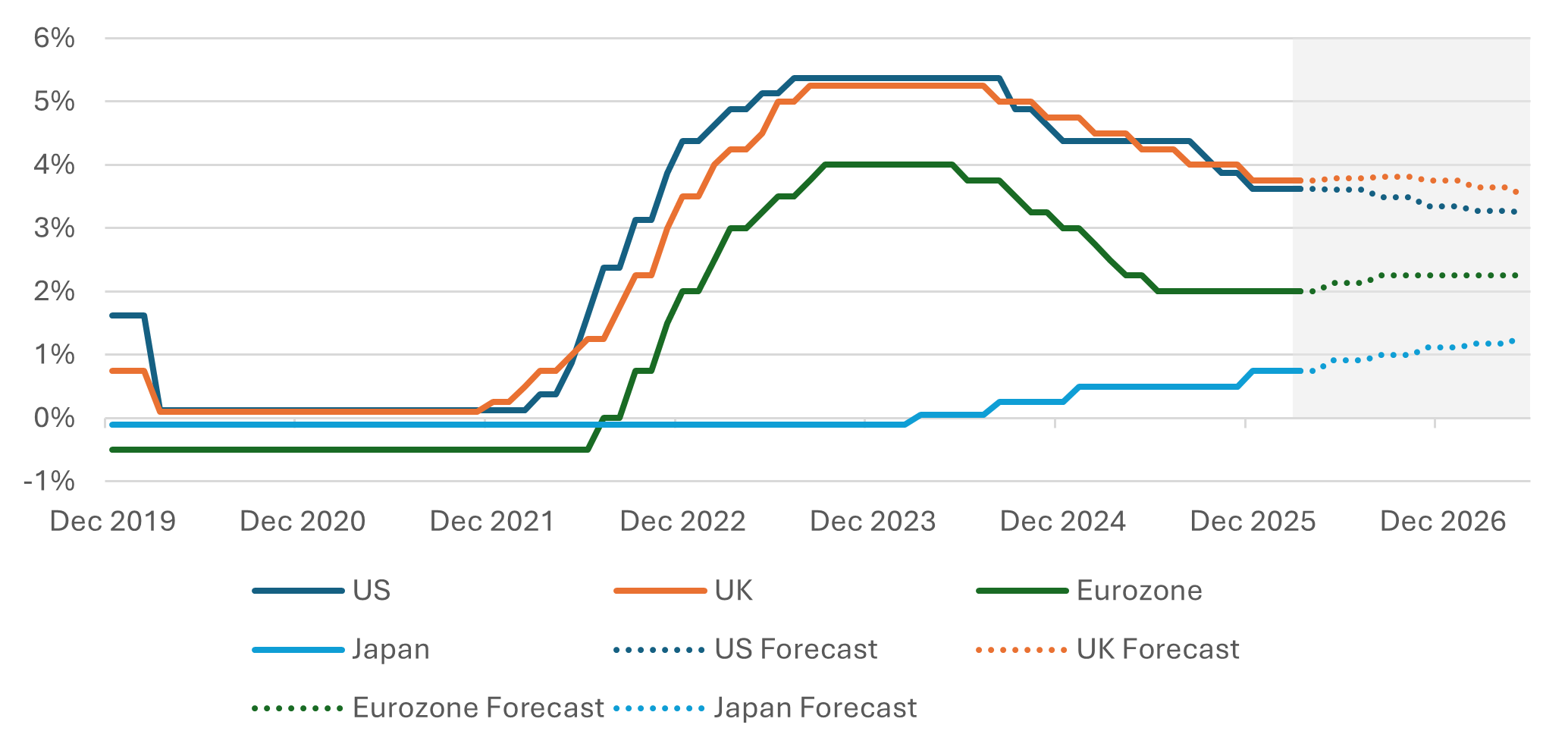

Bonds still lower but have stabilised

Government bond markets seem to be somewhere in between stocks and commodities in recent trade, albeit closer to commodities, as the expectation of potentially lower growth has to some extent offset the expected rise in inflation. Before the start of the conflict, the Bank of England (BoE) had been expecting inflation to fall to around its 2% target in April and derivatives markets were pricing two rate cuts this year. Now, these markets are pricing two increases which would take the current 3.75% base rate to 4.25%. Depending on where oil prices end up and where inflation moves to, we are more cautious on rate rises than market pricing suggests. Our view would be more aligned to that of economists’ forecasts, rather than market pricing, the consensus for which is shown in chart 9 below.

The European Central Bank (ECB) is expected to raise rates twice, according to derivatives markets, which would take its overnight deposit rate to 2.5%. A lower path is expected from the Federal Reserve, which is now seen as having a 20% probability of a single cut by year end. This is partly due to the expectation that Kevin Warsh — the nominee to replace chair Jay Powell who has publicly made the case for lower rates — will be more inclined than his predecessor to implement a lower-rate environment.

Chart 9: The Middle east conflict has altered the future central bank rate expectations, according to economists surveyed by Reuters.

Source: LSEG Datastream, Quilter Cheviot Limited, 23/4/2026. Past performance is not a reliable indicator of future results. The value of investments and the income from them can go down as well as up. You may not get back what you invest.

Although bonds are still notably lower than they were pre-conflict, high starting yields mean that there would need to be a significant further yield rise for investors to lose money by year end.

The case for diversification

The varied response to the Middle East conflict across different asset classes, sectors and geographies demonstrates the value of diversification in times of uncertainty and heightened volatility.

Chart 10: History shows the variability of asset class returns year on year

Source: Morningstar, Quilter Cheviot Limited, 28/4/2026. Past performance is not a reliable indicator of future results. The value of investments and the income from them can go down as well as up. You may not get back what you invest.

A diversified portfolio comprised of different asset classes, sectors and geographies is less susceptible to the swings of any one market. This can be particularly valuable in helping to maintain a more consistent performance during periods of economic uncertainty, like the one we are confronted with today.

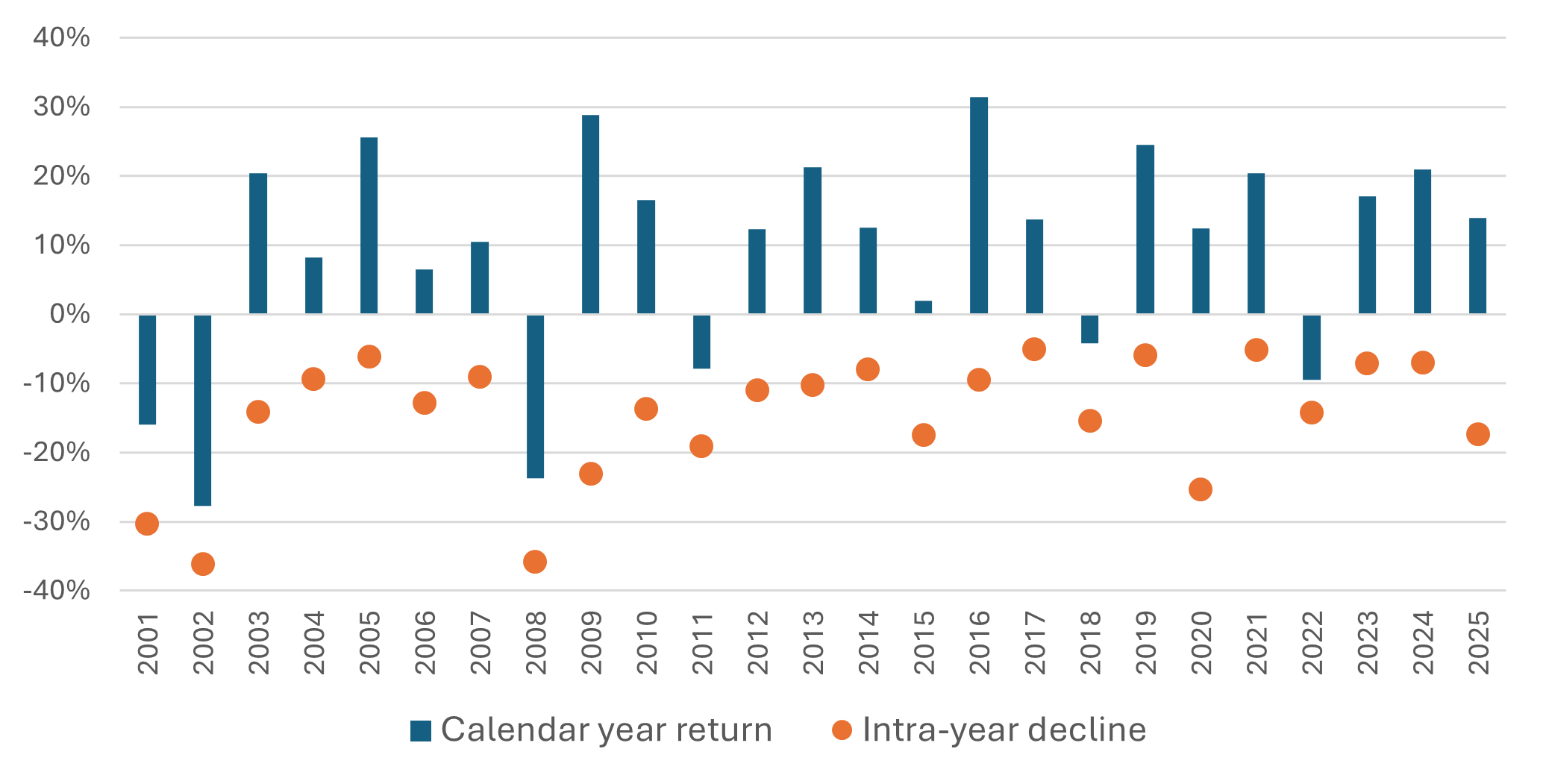

Volatility is uncomfortable but not unusual

We recognise that periods such as the past couple of months are uncomfortable for investors, but they are not unusual. The MSCI All Country World index has experienced an intra-year decline in excess of 10% in 15 of the last 25 calendar years and on only three occasions has the index ended the year down 10% or more.

Chart 11: Most years global equities experience a notable drawdown (shown by the MSCI All Country World Index) even if they finish higher

Source: LSEG Datastream, Quilter Cheviot Limited, 31 December 2025. Past performance is not a reliable indicator of future results. The value of investments and the income from them can go down as well as up. You may not get back what you invest.

We believe it is of the utmost importance to cut through the headline noise and maintain a clear focus on market fundamentals. Although US stocks have recently reached new all-time highs, the gains have not been accompanied by signs of overexuberance — often an indication of unsustainability. Rather, the rise to record highs has been underpinned by strong and improving earnings and earnings growth expectations. The AI race continues to be a major theme, and although there is plenty of uncertainty as to who will be the ultimate winners and losers, it is clear that chipmakers are posting large, rising profits. In fact, US earnings growth has been so impressive in recent months that, along with a largely sideways market, price/earnings valuations on US stocks have fallen.

The overall picture could change but while US companies are experiencing such strong earnings growth, it is only natural that stock prices move higher. Events such as the announcement of large US trade tariffs and war in the Middle East have, thus far, had a relatively muted impact on earnings and unless that changes then there is little fundamental reason to suggest that they will significantly weigh on the stock market.

Conclusion

Stock markets have shown a pleasing level of resilience in recent weeks despite the ongoing energy supply disruption and while bonds and commodities don’t seem quite so rosy, they have at least stabilised. The swift snapback in stocks once more demonstrates the value of remaining invested and taking a long-term approach, with US equities hitting all-time highs even though uncertainty surrounding the Middle East remains.

While we welcome the recent market recovery, we are guarded against complacency and realise that although things look more favourable another negative shock could be just around the corner, either from the Middle East or elsewhere. Corrections to equity markets would be expected should the oil price stay elevated and growth materially damaged. However, in that case bonds would likely rally, on lower growth backdrops, and portfolio diversification effects will provide some cushion through the short-term impact.

History suggests staying invested through such shocks is the better investment approach through time. This is why we maintain our steadfast belief in maintaining a long-term perspective, grounded in fundamental analysis.

There is yet to be an event, including wars, financial crises and pandemics from which the markets have not recovered, and history suggests that looking through the daily headlines and focusing on fundamentals and an investment strategy aligned to risk tolerance and time horizon remains the most reliable approach.