The page you were trying to view is not available for your role and region.

Yet another article with tech bubble 2.0 in the title suggests little has changed since our last piece ‘Tech bubble 2.0?’ published in October 2025. Back then technology stocks, especially those at the centre of the artificial intelligence (AI) trade, were powering ahead and dragging markets higher with them. Cue talk of a tech bubble 2.0 and comparisons with the dotcom boom around the turn of the millennium.

Certainly, at the headline level at least, little has changed since October 2025. Technology stocks have continued to lead stock markets higher; the sums being invested in data centres (facilities built to train and run AI models) and compute capacity have continued to rise—capex increased 70% in 2025, is expected to grow 80% in 2026 and by a further 30% in 2027; and Magnificent Seven Big Tech stocks still dominate the main US index—at the last count, the seven accounted for around a third of the main US market’s value. Not much to add to the original article then? Not at all. Scratch beneath the surface, and the AI narrative has moved on.

The huge amounts being spent on data centre capacity are not the only sums growing at pace. So too, are the AI-generated revenues of the big spenders. Usage of AI in the workplace has also soared. And while the technology sector as a whole has maintained its market leadership, at the stock level, the usual suspects, aka the Magnificent Seven (Alphabet, Amazon, Apple, Meta, Microsoft, Nvidia and Tesla), have not led the charge. Semiconductor (microchip) equipment manufacturers, memory chip producers and power chip companies have been the ones in demand.

Revenue growth, rocketing usage and a switch in leadership, all point to an AI trade that is maturing.

The state of play

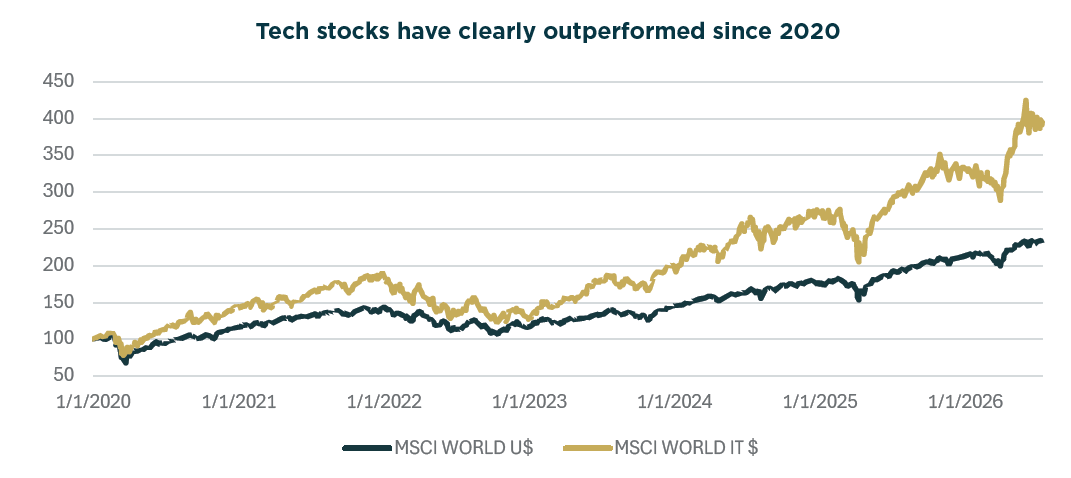

Source: LSEG Datastream, Quilter Cheviot Limited 15/07/2026.

These figures refer to the past and past performance is not a reliable indicator of future results.

As the chart above shows, technology stocks’ outperformance is now in its sixth year. In terms of timeline, the AI trade was triggered by OpenAI’s launch of ChatGPT in November 2022. Then there was the controversy of the Jan 2025 release of Deepseek — an app that trained AI-models for a fraction of the cost of training a conventional model. There have been wobbles along the way, the tariff tantrum in April 2025 a standout here. Overall, enthusiasm for the AI-trade has come hand-in-hand with elevated volatility.

Show me the money!

The Big Four hyperscalers (large-scale providers of cloud-based services including software and data that run on the internet)—Alphabet, Amazon, Meta and Microsoft—plan to spend US$800bn on building data centres in 2026 to power AI initiatives including the large language models (LLMs) being developed by the likes of Anthropic and OpenAI. Next year, the combined Big Four spend on AI infrastructure could top US$1tn.

The trillion-dollar-question then is this, when (if ever) will the huge investments being made start to pay off and generate meaningful tangible returns?

A reality check

We are still early in this journey, however, the key is to ensure reality and expectations match. Does what’s happening on the ground warrant the hype and share price gains? Researching and analysing how the AI trade is evolving plays an important role here and below is a checklist of metrics and developments we are keeping a close eye on:

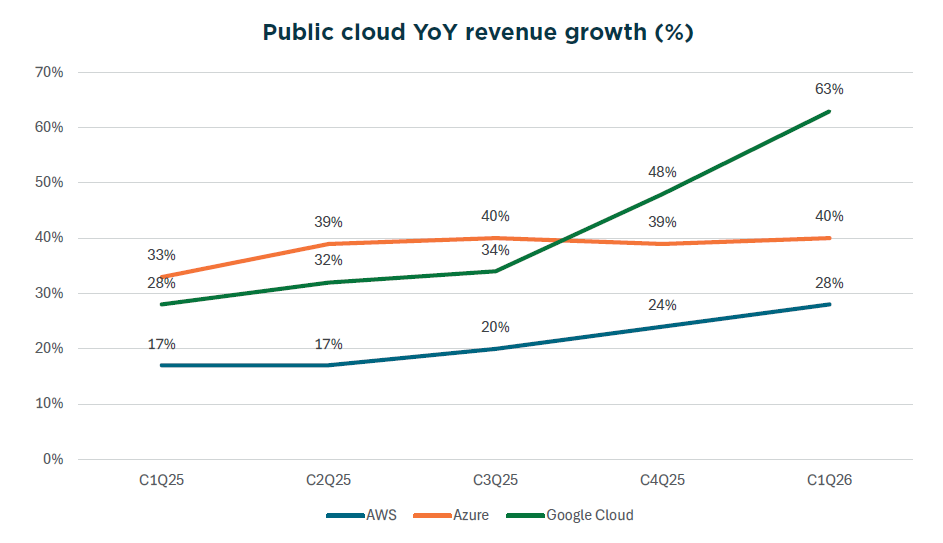

- Growing AI-based revenues: Three out of the Big Four hyperscalers have extensive cloud businesses—Amazon, Alphabet and Microsoft— and all three posted stellar growth in cloud revenues in their recent Q1 results. Alphabet saw its cloud revenue growth soar from 48% to 63% so that Q1 revenues came in at US$20bn, while the order book backlog jumped from US$240bn to US$460bn. Similarly, Amazon’s Q1 cloud revenue growth rose to 28% from 24%, as revenue hit US$37.6bn; meanwhile, revenue growth at Microsoft ticked up to 40% from 39% with revenues reaching US$34.7bn. Spending on data centres is leading to faster hyperscaler cloud growth.

Source: Amazon, Microsoft and SEC, Quilter Cheviot Limited, 15/07/2026.

These figures refer to the past and past performance is not a reliable indicator of future results.The benefits of AI are also showing up in digital advertising revenue growth. At Alphabet, search revenue came in at US$60.4bn in Q1, a 19% increase on last year. Meta’s advertising sales soared 33% to US$55bn in Q1, the fastest rate of growth seen in five years. The reason for the spike in revenues, AI. Both Alphabet and Meta are using the technology to help advertisers maximise the returns they make on their investments by refining ad targeting and improving user engagement. This in turn is generating higher ad spending.

It is not just the hyperscalers that are reporting strong revenue growth. So too are the LLM developers themselves. Based on run-rate revenues, Anthropic’s annualised recurring revenues exceeded US$40bn in May, a fourfold increase since the turn of the year. The comparable number for OpenAI is US$30bn.

Takeaway: AI is already generating revenues, and these are growing fast providing a return on investments made to date.

- Soaring token consumption: Revenue growth at the LLM developers is being driven by increased usage of AI by companies and their employees. The use of tokens (the basic units of output from LLMs), or token consumption, however, has grown to such an extent that companies are having to introduce caps on the amount of tokens their employees consume to keep a lid on costs. Companies will likely put guardrails around usage going forwards similar to the way cloud deployments were optimised around 2022.

Takeaway: AI revenues and usage are growing rapidly but keep an eye on token cost and value as companies look to control costs. Lower corporate AI usage could impact the pace of revenue growth at LLM developers however we believe there is still considerable run room for increased adoption of AI.

- Broadening out of the AI trade: For much of the past five years, it’s been the Magnificent 7 Big Tech stocks that have led markets higher. Since the turn of the year, however, Nvidia and co have largely traded sideways. Instead, it has been other semiconductor stocks that have caught the eye, particularly memory companies such as Micron, Hynix and Samsung; semiconductor capital equipment companies such as ASML, KLA and Applied Materials and power chip companies such as Infineon. All those data centres being built require chips and lots of them.

Takeaway: There has been a switch in investor focus away from the big spenders to their suppliers, such as chipmakers. The change in leadership could be viewed as investors focusing on those companies that are showing a clear revenue acceleration because of AI. The key point from the chart above is investors are buying the companies that are seeing revenue acceleration from AI i.e. the semiconductor companies.

- Trillion-dollar IPOs (initial public offerings): The successful US$1.75tn+ market debut of Elon Musk’s SpaceX promises to kick off a spate of trillion-dollar IPOs, notably those of Anthropic and OpenAI. The concern is that owing to the size of these new issues existing large and liquid tech names will face selling pressure as funds will have to be raised to acquire stakes in the newcomers. Importantly, however, SpaceX’s 5% initial free float and similar expected floats at Anthropic and OpenAI should limit the scale of any selling.

Takeaway: The fear that the trillion-dollar IPOs will generate selling pressure is a genuine concern but is arguably overstated.

- Valuations: Bubbles are typically associated with high valuations. Although the technology sector trades at an approximate 20% valuation premium to the main US stock market, this premium, in our view, reflects the superior growth available from technology stocks. Furthermore, tech valuation multiples are significantly below those seen at the peak of the dotcom bubble in March 2000.

Takeaway: Share price gains to date have been underpinned by strong forecast earnings growth and positive earnings revisions. For example, earnings in the global information technology sector within MSCI ACWI are forecast to grow 70% in 2026 and 31% in 2027. Forecasts and estimates are based on current expectations and assumptions and are subject to change. Actual outcomes may differ materially.

Summary

With AI-generated revenues growing rapidly, the technology being widely deployed by corporates around the world and a switch in leadership away from the Magnificent 7 to those companies experiencing strong AI-driven revenue acceleration, such as semiconductor stocks, the AI trade is broadening out and maturing.

As with all transformative technologies, however, risks remain. With this in mind, our strategy remains grounded in reality rather than euphoria. This is why to date we have largely favoured suppliers such as the chipmakers and semiconductor equipment manufacturers that are currently enjoying (and are expected to continue doing so going forward) favourable demand/supply dynamics.

We will maintain this prudent approach to investing in the AI trade, even though it is clearly showing signs of maturing. For evidence of this, look no further than the change in emphasis in the metrics being used to measure progress, both real and expected. Previously it was the ambitious capex plans of hyperscalers that dominated the headlines. Now, the headlines are shared with AI-generated revenue and earnings growth as well as token cost and value. All indicators you would expect to see gain prominence as the AI trade matures.