The page you were trying to view is not available for your role and region.

The pace and scale of global mobility have accelerated in recent decades. Why? A number of reasons: employment, lifestyle change and retirement. Regardless of why more people are on the move, those with cross-border lifestyles, or arriving in countries anew, face increasingly complex regulations, laws and systems of taxation. That’s not all. Political agendas such as Brexit have had far-reaching consequences too. As has COVID-19 and more recently, war in the Middle East which has seen large numbers of people, particularly expatriates, displaced. Planning (financial or otherwise) for a move overseas has never been easy but it seems today it has never been more challenging.

With no two individuals and their circumstances the same, personalised advice is invariably required. Nevertheless, at least within the international tax system, there are a number of key themes which can help guide our thoughts for private clients.

Tax system models

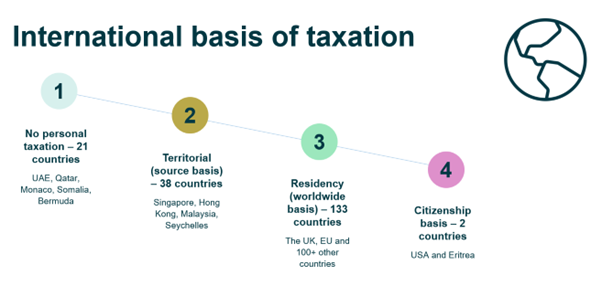

Broadly speaking, income and gains tax systems can be divided into four categories:

No direct taxation: 20 countries have no direct taxation, in other words residents do not suffer tax in that country on locally derived income or gains, or on foreign income or gains in the country in which they live. Well-known amongst these are the United Arab Emirates (UAE), Oman, Qatar and Monaco.

Source-based: Another 38 countries employ what is known as a source-based (also known as a territorial) system. Here, only local income and gains, from a source inside that country, are charged tax there. Examples include Singapore and Hong Kong.

Residency-based: The largest category with 133 countries, including most of Europe, is a residency (or worldwide) based system. Here, residents of a country are taxed on their worldwide (local and overseas) income and gains. Such income and gains are, in most situations, taxable even if not remitted back to the country of the taxpayer’s residence.

Citizenship: At the other end of the spectrum sits the United States (US), where not only are residents taxed on their worldwide income and gains, but also non-resident citizens worldwide, including on their income and gains not from the US. This is known as taxation by citizenship. It’s probably this situation that contributed to the need to implement the Foreign Account Tax Compliance Act (FATCA), which since 2016 has required that foreign financial institutions and certain other non-financial foreign entities to report on the foreign assets held by their US citizen account holders to the Internal Revenue Service (IRS). Only one other country taxes their citizens worldwide similarly, that being Eritrea in East Africa.

While there are four different types of tax system, in reality there is an almost infinite number of subtle but important variations amongst the 195 countries that the United Nations recognises across five continents.

Spot the trend

In the diagram above, the trend over recent decades has been for country systems to move from the top left to the bottom right. However, although no extra countries have formally become citizenship-based, there are a number of locations that have some of those qualities, because of their wide definitions of tax residence. For example, many South Africans overseas have retained their ‘ordinarily resident’ status. This common law nuance can easily mean that they are fully beholden to the tax system there, without any benefit for their contributions. The same could be said for Chinese overseas. Following recent tax reforms and enhanced guidance, it is clear that those retaining their domicile or ‘hoku’, (household registration) need to declare and pay ‘individual income tax’ (a tax that applies to gains as well as income) whether income or gains are remitted back to China or not, given the world’s most populous country employs a residency-based system.

Increased transparency, through the Common Reporting Standards (CRS), is increasingly allowing tax authorities to track, trace, collect and sometimes criminalise transgressors.

Double taxation

Because of the lack of tax harmonisation, variations create the potential for double taxation (where the same income or gains are taxed by different countries). Double tax treaties (also known as double tax agreements, or DTAs) which many countries enter into with each other, are designed to alleviate such possibilities. However, just like taxation, these aren’t always logical or consistent.

Occasionally double tax treaties facilitate double non-taxation, where income or gains are not taxed at all. ‘Treaty shopping’ is the name given to those who attempt to exploit such mismatch.

Death duties

It should be noted that the application of estate duties and inheritance taxes are often subject to significantly different rules, with individuals frequently unaware of their obligations, and very few double tax treaties to compensate. International law defines estate taxes as chargeable according to the estate of the deceased, often relating to their domicile or citizenship, whilst inheritance taxes relate to the value an individual beneficiary receives, and their personal circumstances, rather than that of the donor. In other words, the former is a donor-based tax, the latter recipient-based.

It is also worth noting that residents and citizens of a country where there is no death tax can still see a liability emerge if wealth is situated in a country where the tax applies, and examples of this include ownership of UK or US stock.

For example, a Singapore parent leaving wealth to a Singaporean heir might expect death taxes not to apply, as death taxes were abolished in Singapore in 2006. However, above the Nil Rate Band (NRB) exemption of £325,000, the deceased’s UK shares could be subject to a 40% liability, and above just US$60,000 a US liability on US wealth for the same client (even if held on an overseas banking platform) of between 18 and 40%.

The UK has just ten double tax treaties* for IHT, and US has 16**. Whilst unilateral relief might be available, this should not be relied upon.

Long-term residents of the UK (formerly known as domicile) will note the system they are beholden to has the characteristics of an estate tax but is confusingly known as an inheritance tax (IHT)! Given three name changes and regimes in less than 50 years, it is perhaps unsurprising that the UK Office of Tax Simplification in 2015 rated UK IHT as the third most complex tax out of 107 taxes considered.

* Inheritance tax double taxation relief

** Estate gift tax treaties International

Planning opportunities

In the above-mentioned situation for IHT, purchasing UK or US securities through an insurance bond as opposed to a conventional banking or proprietary trading platform ensures the policyholder is detached from the underlying asset. This should apply equally to any owner from a country outside the narrow range of DTAs the UK and US have, and even some where there is a DTA, but the UK or US has a higher rate than where the individual is domiciled.

Regarding income and gains on investments, for those who are residents of countries subject to taxation according to their residency (a worldwide basis), which make up over two thirds of all countries, there is a clear distinction between owning wealth directly or on a conventional trading platform compared to through an insurance bond. Normally, through direct ownership or through a trading platform, for tax purposes the liability on income and gains occurs annually as they arise, often even if not remitted to where they live.

When held through a bond, all income (dividend, coupon, rent and interest) as well as on gains when holdings are realised within the bond, do not give rise to a liability at that point in time. This principle is known as gross roll-up.

Three reasons why gross roll-up can be valuable:

- tax-deferred means tax on profit that would have been deducted annually works for the investor for longer before it becomes chargeable.

- savings can be significant if a policyholder’s tax rate drops, or they move to a country where tax rates are lower, is source-based or charges no tax.

- for an arriver into the UK (from any other country), full credit is given for time spent overseas, known as time apportionment relief, meaning almost the full value of profit can legitimately be removed from personal taxation. However, because the new UK Foreign Investment and Gains legislation does not apply to bonds, a better outcome for arrivers who have been absent for typically 10 years, may be available without employing a bond.

Wealth transfer

How clients can pass on their wealth depends on the laws of the country where they and their wealth are situated, which can make succession planning challenging, yet many investors are blissfully unaware of the difficulties they will leave their loved ones. For individuals subject to common law, wills, trusts and nominations are effective in helping clients to retain control over their wealth and potentially manage IHT.

Trusts can be used with insurance bonds to ensure wealth is distributed in line with the policyholder’s wishes quickly (without probate) and confidentially (unlike wills which are public knowledge following death). The same is true for beneficiary nominations with insurance bonds, with the additional benefits that the policyholder retains control in their lifetime, can easily change their mind, and without the additional cost associated with trusteeship.

Where the common law doesn’t apply, there may still be scope for using trusts and policy nominations with insurance bonds, according to the individual’s citizenship and location of their wealth, with appropriate financial and/or legal advice.

Conclusion

As ever, the devil is in the detail, but the value of an adviser is in understanding how these subtleties and nuances, combined with the product options available, can become meaningful tax-planning solutions, in ever-changing cross-border situations.

This material is not tax, legal or accounting advice and should not be relied on for tax, legal or accounting purposes. Quilter Cheviot Limited does not provide any tax, legal or accounting advice. You should consult your own tax, legal and accounting adviser(s) before engaging in any transaction.