The page you were trying to view is not available for your role and region.

Tesla’s second quarter results painted a challenging picture for the world’s largest electric vehicle maker. Slowing sales, rising costs from employee lay-offs and investments in artificial intelligence (AI) infrastructure and an official postponement of the planned unveiling of self-driving taxis, known as “robotaxis”, caused an initial negative reaction in the share price.

Tesla is not currently a holding in any of our Managed Portfolio Service (MPS) strategies.

Reduced pricing and a 5% decline in sales volume for the Model S/Y contributed to a 6% drop in automotive revenues for Q2, putting significant pressure on operating margins which fell 333 basis points to 6.3% — comfortably lower than the 7.6% expected and ranking among the lowest in the automotive industry.

There was little on the earnings call to assuage concerns in this regard, with Tesla refraining from reiterating previous guidance on growing automotive units this year and instead highlighting ongoing margin pressures due to potential European tariffs and new financing programmes aimed at boosting demand.

Under strain

Tesla’s core automotive business is clearly under strain, and it’s no surprise that Elon Musk is shifting focus towards AI. We see no immediate catalyst for a material improvement in the second half of the year and Tesla’s ability to post a positive free cash flow for 2024 is being seriously questioned.

The introduction of lower-cost models, announced in Q1, will not see meaningful availability until the second half of 2025, raising concerns as to whether these model refreshes will stimulate demand sufficiently to significantly improve the outlook, especially with the intensification of competition in key markets such as China. Furthermore, these models could further dilute margins while the potential removal of IRA (Inflation Reduction Act) poses a threat to Tesla’s cash generation capabilities, an essential characteristic for funding its ambitious AI initiatives.

Over a quarter of total capex spend (US$2.3bn) is currently going on AI infrastructure (US$600m) and while free cash flow was positive in the second quarter, for the first half it remained in negative territory due to the major inventory build being only partially reversed and accounts payable drawn down.

Given these challenges we remain cautious and although the stock performed fairly well in the first six months of the year on bullish AI sentiment, the year-to-date return is back in the red after the latest results. We believe the underlying pressure on Tesla’s auto business cannot be ignored, which is particularly concerning for the company’s growth prospects. Therefore, we favour remaining on the sidelines for now.

Our MPS active management

Access to active management is a key attraction of a model portfolio service (MPS), offering several potential advantages in terms of flexibility, returns and risk management. Tesla has not been a holding in our MPS strategies since 2022, despite being one of the largest components of US equity benchmarks and a member of the so-called “Magnificent Seven” tech stocks. The rationale for this is outlined above, with the decision to not include the stock taken by our portfolio managers after consultation with our in-house stock selection committee and Mamta Valechha, our equity analyst specifically covering the stock. This is not to say that we think Tesla is a poor company, we just believe that at present there are more attractive opportunities elsewhere and our “Building Blocks” structure allows us the flexibility to make these decisions precisely and swiftly.

About our “Building Blocks”:

- Our strategies are constructed solely using our ‘Building Blocks’ — eight purpose-built funds specifically designed for use within Quilter Cheviot’s MPS. This allows a far greater degree of active management without burdensome costs, as we can select individual securities and fine tune holdings to our desired exposure.

- Quilter Cheviot is both the MPS model manager and underlying manager to these funds. This means changes to the underlying holdings within each Building Block can be implemented at the fund level in a dynamic manner. Changes are immediately reflected across all holders, preventing the need for a portfolio rebalance and all the accompanying operational complexity created by a ‘traditional’ MPS. Quilter Cheviot does not charge a management fee for the running of the Building Block funds, removing any conflict of interest - the funds are solely to enhance the investment proposition.

- The Building Blocks reflect our highest conviction investment views and they go beyond open-ended funds. They can invest in direct equities, direct bond holdings, exchange-traded commodities (ETCs), and closed-ended or exchange-traded funds (ETFs), irrespective of the wrapper in which a client’s portfolio is held.

Passive funds are only considered judiciously, for instance as a temporary home for flows or a targeted exposure to a specific index, instead of being relied on as a tool to lower costs. This avoids the pitfall of diluting active exposures and alpha-generating potential.

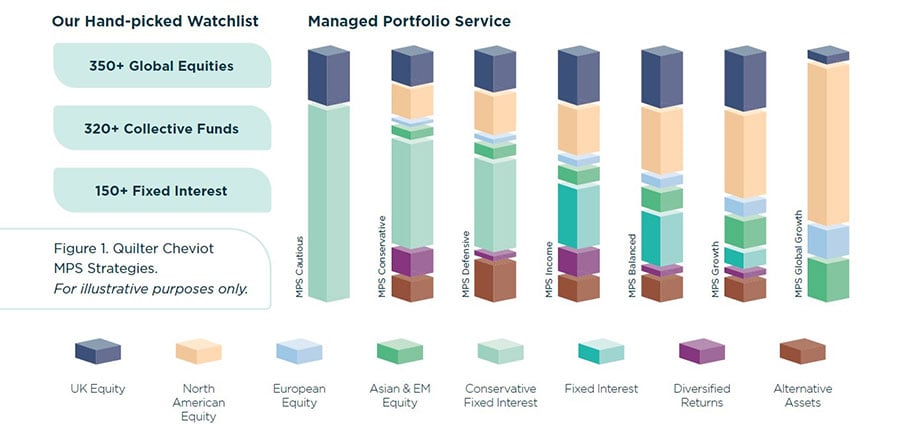

See Figure 1 below for an illustration of how these funds are used across our MPS strategies

Figure 1. Quilter Cheviot MPS Strategies.

For illustrative purposes only.