The oil price jumped to its highest level since June 2022 in the early hours of Monday 9 March as concerns grow around how long the conflict in the Gulf will disrupt global supplies. Gas prices have also moved sharply higher, and the impact of rising energy prices can be seen further afield with stock and bond markets moving lower in anticipation of the growing potential for a wider inflationary shock.

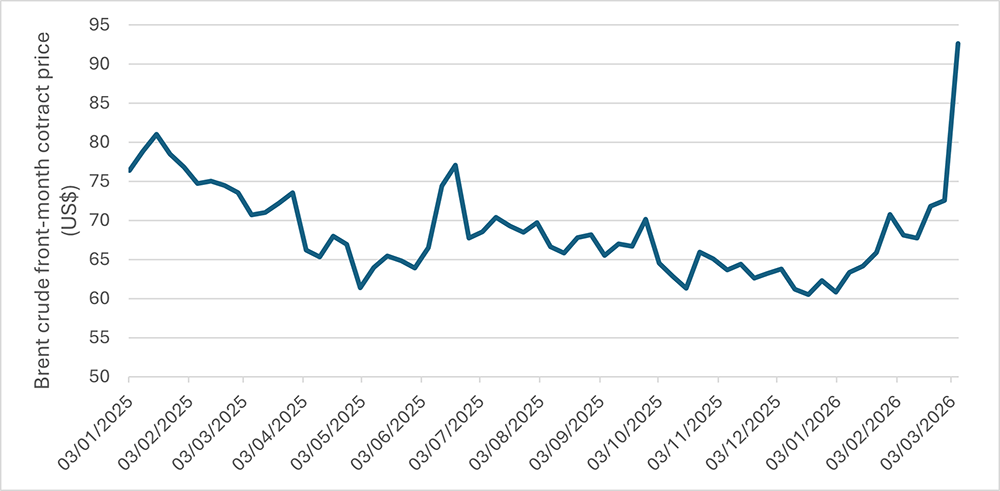

There has been a sharp rise in the oil price since the conflict began on 28 February

Source: LSEG Datastream 9/3/2026. Past performance is not a reliable indicator of future results. The value of investments and the income from them can go down as well as up. You may not get back what you invest.

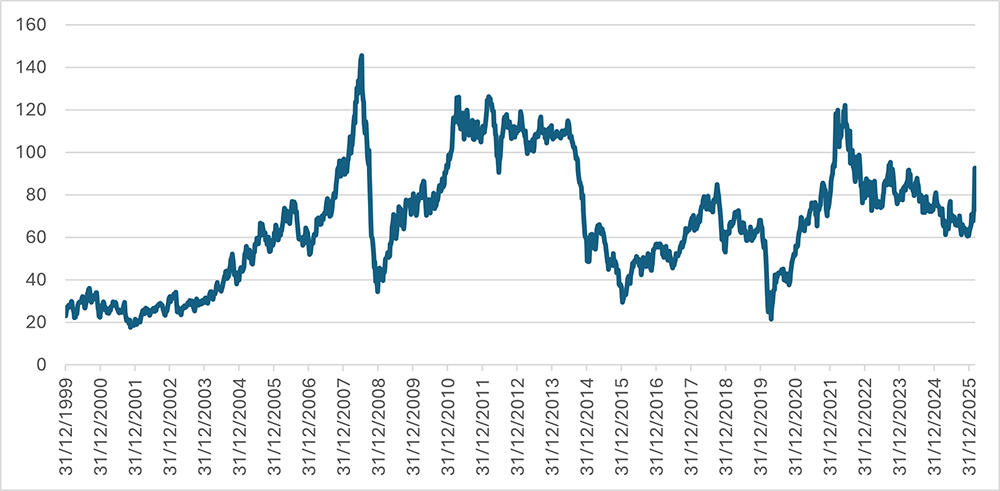

But from a longer-term perspective, the oil price remains below previous peaks

Source: LSEG Datastream 9/3/2026. Past performance is not a reliable indicator of future results. The value of investments and the income from them can go down as well as up. You may not get back what you invest.

Last week Brent crude, an international oil benchmark, rose 27% for its largest weekly gain since at least 1991 after war broke out in the Middle East. Things had been looking more encouraging on the morning of Saturday 7 March after the Iranian president, Masoud Pezeshkian, declared an end to attacks on neighbouring countries. However, a de-escalation sadly did not occur and shortly afterwards missiles and drones were launched against Dubai, Qatar and Bahrain, clearly indicating that the hardline Iranian Revolutionary Guards — who do not want to compromise with the US — are the ones in power and not the moderates.

Markets on Monday 9 March responded negatively to the events, with stocks and bonds lower while the US dollar gained. As was the case last week, European and Asian equities have declined more than US equivalents, in part due to the greater energy independency of the US.

Higher for longer

There is a feeling among market participants that although the sheer military power of the US and Israel means that it remains possible that the Iranian military will ultimately succumb, the feeling now is that this may take much longer than originally expected. For the Revolutionary Guards, their approach to combat and ability to launch missiles and drones from a wide range of locations mean it is now unlikely the Strait of Hormuz — through which 20% of global oil and gas supply pass through — will reopen fully to commercial shipping anytime soon. The Strait of Hormuz is a natural potential chokepoint for energy supplies given that it is just 20 miles wide at its narrowest, so a relatively easy target for drones, missiles and sea mines.

Qatar and Kuwait have started reducing or suspending oil and gas production due to a lack of storage, resulting from the blockage of exports on oil and LNG (gas) tankers. The situation has deteriorated from Friday night when the probability of a swift reopening of the Strait of Hormuz had seemed more possible. It appears a more prolonged closure of the Strait of Hormuz is now more likely, which will mean a higher average oil price in the coming months. The energy sector unsurprisingly outperformed last week, beating the benchmark by 10% in the UK, 12% in Europe and 8% in North America.

SPR release

One of the measures that can be taken to lower the oil price is the release of emergency oil reserves, known as SPR (strategic petroleum reserves). G7 finance minsters are reportedly discussing a possible joint release co-ordinated by the International Energy Agency (IEA). The 32 members of the IEA reportedly hold strategic reserves in the region of 1.2bn barrels and a release of 300m-400m barrels is currently being touted. The effective closure of the Strait of Hormuz is preventing approximately 20m barrels per day passing through, so a 400m barrel release would equate to around 20 additional days of supply. The US and Japan are the two main figures, accounting for around more than half of the reported total stockpile.

Risks to growth and inflation

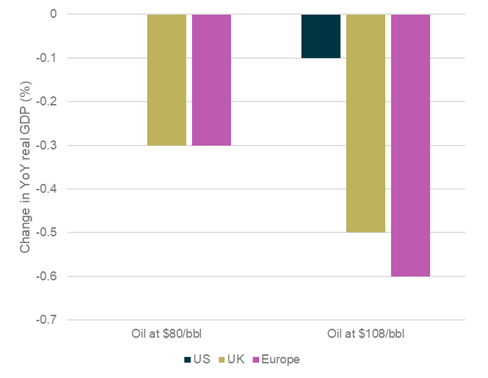

The situation is highly dynamic and circumstances can change quickly, but as a rough rule of thumb we can look at how higher oil prices are expected to impact GDP growth and inflation. This is important because fundamentally stock market returns are mainly driven by growth and/or inflation over the longer term. Taking all else as equal, as you would expect, the higher the oil price the larger the impact (for the below we assumed sustained prices for 3-6 months). Brent crude was trading around US$70 a barrel before the conflict broke out.

Impact of oil shock on real GDP (%)

Source: Bloomberg Economics 2/3/2026. Past performance is not a reliable indicator of future results. The value of investments and the income from them can go down as well as up. You may not get back what you invest.

If oil is around US$80 a barrel for the next few months then the impact is manageable, but should it be sustained around US$108 then the impact is more meaningful. For instance, the Eurozone 2026 GDP growth forecast of 1.2% would be halved should oil remain around that level. This is only accounting for direct, or first order effects, and there may well be knock-on, secondary order effects that also impact growth which are harder to model.

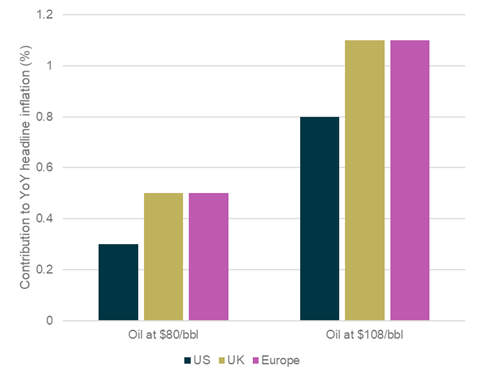

Impact of oil shock on headline inflation (percentage contribution)

Source: Bloomberg Economics 2/3/2026. Past performance and forecasts are not a reliable indicator of future results. The value of investments and the income from them can go down as well as up. You may not get back what you invest.

Similarly, a 50-basis point (0.5%) rise in inflation for the UK and Europe would be detrimental but not too significant, whereas an increase of 100-basis points (1.0%) or more would have further reaching implications and increase the pressure on central banks to raise interest rates.

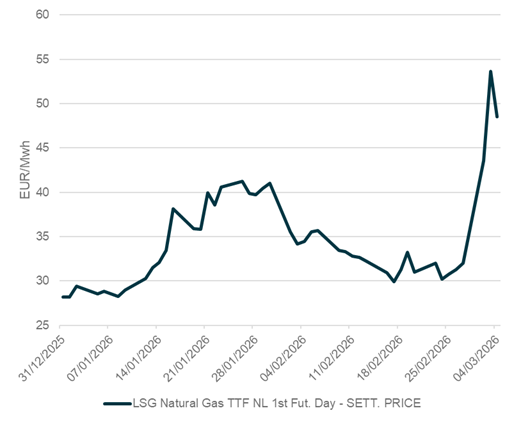

Gas rising but some way off 2022 highs

As we saw with the 2022 Russian invasion of Ukraine, natural gas prices can have a larger impact than oil prices on European energy costs. Gas prices are similar to oil prices in that they have risen but are still not that high in historic terms.

European natural gas price, YTD (Dutch TTL 1st Futures Contract)

Source: LSEG Datastream 4/3/2026. Past performance is not a reliable indicator of future results. The value of investments and the income from them can go down as well as up. You may not get back what you invest.

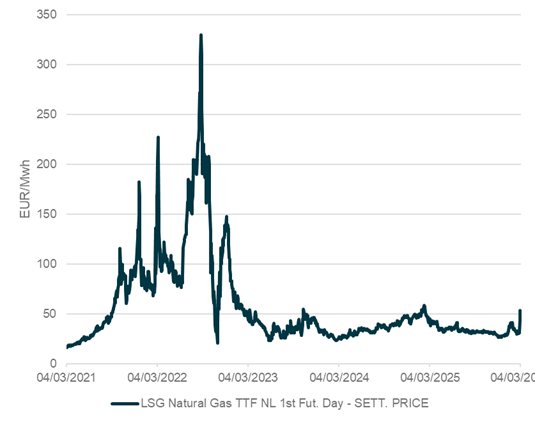

European natural gas price, 2021- (Dutch TTL 1st Futures Contract)

Source: LSEG Datastream 9/3/2026. Past performance is not a reliable indicator of future results. The value of investments and the income from them can go down as well as up. You may not get back what you invest.

It’s not just the direct impact of energy markets that will have further reaching implications. Fertiliser, food and other products such as petrochemicals, plastics and aluminium may all see supply side disruption.

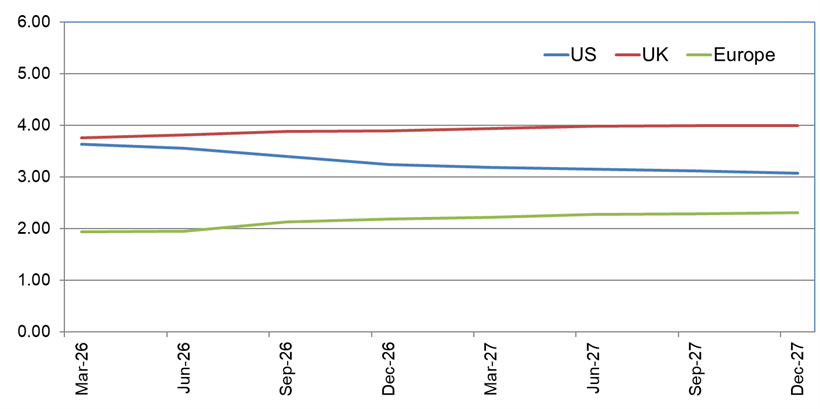

Cuts postponed. Hikes back on the table

The expectations for future central bank rates have moved markedly higher since the conflict began, with forecast interest rate cuts being priced out in derivatives markets and a European Central Bank (ECB) hike now expected before year end.

Source: LSEG DataStream 9/3/2026. Past performance and forecasts are not a reliable indicator of future results. The value of investments and the income from them can go down as well as up. You may not get back what you invest.

An important difference between the current macroeconomic environment and that in 2022 when Russia invaded Ukraine is the position of central banks. Four years ago, central banks had rates still at near record low levels as economic activity snapped back quickly from the Covid-19 pandemic following the release of vaccines. While the conflict undoubtedly contributed to the bout of high inflation that followed, the seeds for it had already been sowed by the extraordinary levels of stimulus during the pandemic (fiscal and monetary) which fuelled demand and the hesitancy with which central banks reacted to both the re-opening of the global economy and the conflict itself by raising rates.

Currently rates are closer to neutral territory than in 2022 when they were lower and more stimulative. The memory of high inflation is also fresh in the mind so central bankers are expected to be far more vigilant in raising rates should we see a prolonged rise in energy prices and inflation metrics.

Conclusion

The conflict in the Middle East has sadly escalated and now looks possible to have a more prolonged impact on energy prices. While the situation can change quickly, the longer oil prices remain above US$100 per barrel, the larger the potential impact on growth and inflation, resulting in further reaching impacts on financial markets. Lower growth and higher inflation are negative for stocks and bonds, all else equal, and a sustained disruption of traffic through the Strait of Hormuz would be felt more widely.

We are monitoring several elements of the market to help us navigate the situation, including the G7 meetings and release of strategic oil reserves and the impact on markets, the scale and scope of energy infrastructure asset targets and the scale and scope of further production cuts.

We believe diversification remains the best way to manage risk. Tactical asset allocation and instrument selection can help navigate high probability smaller risks but low probability events with high impact, or unforeseeable risks, are managed best through multi-asset diversification. While the current situation in the Middle East appears to have escalated and the risks have risen, we believe it is of utmost importance to maintain a long-term perspective and not make knee-jerk reactions. There has yet to be an event from which markets have not recovered, including World Wars, financial crises and pandemics. The best way to try and generate consistency of returns through time, in the face of a world with continual risks, is an investment process without emotional reactions, paired with an awareness of the clients’ risk profiles and time horizons.