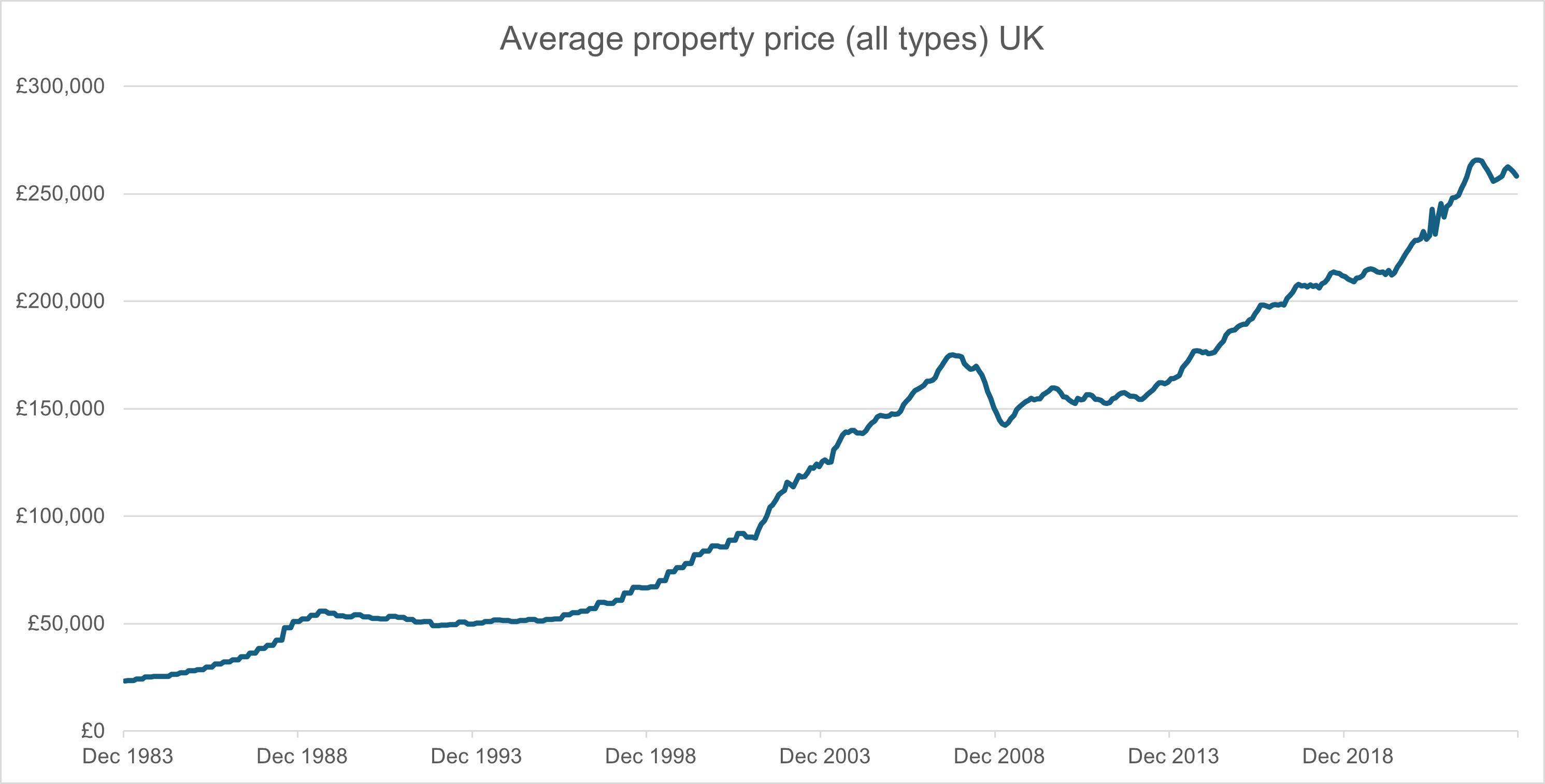

If you think of investing as a beauty parade where different asset classes (equities, bonds, property etc) vie for the investor’s attention (and cash), then property arguably has a head start over the rest. Property is more familiar. You can touch a house. Unlike share certificates, which are today largely held electronically. Most people have firsthand experience of the returns a property can generate, be it price growth and/or rental income. And then there are those stories of how parents or grandparents paid ‘just’ £30,000 for their first property 40 or so years ago, around a tenth of today’s average property price of around £300,000 (see chart below).

It is easy to see how property can capture the imagination of investors after viewing a chart like this. It is also not hard to see why over 40% of respondents taking part in the 2024 English Private Landlord Survey ticked the ‘preference for investing in property’ and ‘contribute to pension’ boxes as the main reasons why they became landlords. The question is, have they been drawn into a myth: that property investment beats allcomers?

Myth#1: History shows property is a good investment

If you don't know the actual total return, how do you know whether property is a good or bad investment?

Based on the above chart, between 1980 and 2025 property generated an annualised return of around 6.3%. A decent number. The thing is the average property investor is unlikely to have locked in a 6.3% total return each year. That’s because the graph above simply charts price growth at the headline level. It does not include all the various costs, both monetary and time-related, that come with investing in property, not to mention the interest on any borrowing, or after-tax rent.

Because of these variables, the total return on property is not an easy number to come up with. In all, eight factors need to be taken into account, according to a 2016 paper by David Miles, Professor of Financial Economics at Imperial College London. As well as the annual change in the value of the property and gross rent, there are ongoing annual expenses, mortgage size, interest paid, and purchase costs (stamp duty, legal fees) to consider. Professor Miles offers up a total-return formula:

R = (1-tax) x [RENT + CG - exp - rm x M - FC/T]

- Annual gross rent on a property = RENT

- Ongoing annual expenses (e.g. repairs, maintenance, administrative costs, insurance) = exp

- Fixed cost of a purchase and sale (e.g. stamp duty, estate agent fees, legal fees) = FC

- Size of mortgage = M

- Current value of property = P

- Mortgage relative to price of property is leverage = lev (so lev = M/P)

- Interest rate on mortgage = rm

- Capital gain (change in value of property over a year) = GC

- Horizon over which the fixed cost of buying and selling a property are spread = T

The takeaway? It is likely even those landlords with a preference for viewing property as an investment do not know the actual total return generated.

Myth#2: Property outperformed stock markets between 1980-2025

Even using the inflated annualised return of 6.3%, property has underperformed London’s large cap stocks with dividends reinvested.

As for how other asset classes compare, once again not all is as it seems. Using large caps on the UK stock market as a comparator and property’s 6.3% annualised return as the benchmark, the large caps’ +5.3% annualised return between 1980 and 2025 falls short. But remember the property figure does not include all eight of Professor Miles’ factors. Jury still out then? Not necessarily, for that 5.3% stock market return excludes dividends received. That’s important because dividends make up a large portion of stock markets’ historic returns. If dividends received are reinvested into stocks, the annualised return of UK’s large caps jumps to +7.4%, comfortably above property, before borrowing costs, rent etc are factored in.

Myth#3: Property lets you sleep better

There may be a perception that property prices only ever go up, but they don’t. In the not-so-distant past there have been steep drops and long recovery times.

There is a view that property exhibits lower levels of volatility compared to other asset classes. Back to the chart above showing the performance of the average property price over the last 40 years. At least two down periods stand out.

The first starts in the summer of 1989. August 1989, the average property price was £60,700. Over the next 38 months, the price fell 12% to £53,200. A 12% drawdown stacks up well against those that stock markets can suffer from. Less so, when you consider it took 7.5 years for prices to recoup the lost ground - the average property price only got back to 1989 levels in 1996.

The other material down period took place in October 2007 when the average property price was £189k. In just 18 months this fell 18% and only returned to 2007 levels in July 2014, seven years later.

Myth#4: Property investment is easy to understand

The tax regime surrounding property investment has become more…taxing. Perhaps one reason why more landlords have been reducing their exposure - over 30% of landlords were looking to reduce their exposure to the property investment market in 2024, almost double the 16% in 2018, according to the 2024 English Private Landlord Survey.

Courtesy of Professor Miles, we have already seen how calculating the total return of a property investment is easier said than done. But if you think that’s complicated, try getting your head around the world of property taxation.

Question: How many changes to property taxation were there over the nine-year period from 2012 to 2020?

Answer: 22, the vast majority of which have been negative, meaning taxation has not just become more complicated but far less generous to landlords too! These changes include the removal of the wear and tear allowance, the phased removal of mortgage interest tax relief and multiple changes to SDLT (stamp duty land tax). And it’s not just a matter of understanding what these changes mean, but also knowing when they come into force. Not all came into effect on 6 April, the beginning of the new tax year, as you might expect, but 4 December, 1 January, 4 August, 1 April too. And some tax liabilities are triggered at different stages of the transaction process. For capital gains tax (CGT), the key date is normally exchange; for SDLT, normally completion.

Myth#5: It’s best to hold property investments in a company

A corporate entity may make sense for those buying a property, less so for those who already own properties.

Owning a property through a corporate entity does offer benefits. Companies enjoy tax reliefs on interest payments for example. But for landlords who already own one or more properties, moving these from private to corporate ownership poses challenges. Taxes are charged both on entry into and exit from the company. There are reliefs available for CGT deferral and SDLT, but to qualify landlords typically have to demonstrate they have been running a genuine portfolio of properties as a partnership for several years and that they have been spending half a working week managing those properties. Advice, another cost, is definitely required.

A further point to bear in mind is that very few debt providers will allow a buy-to-let or residential mortgage to sit within a corporate entity. So, it becomes difficult to move a property with debt attached into a corporate structure. A corporate finance loan could be taken out but these can be expensive.

More than meets the eye

There are so many variables associated with property investment that it is unlikely the average investor would have been aware of, let alone understand, all of these before investing. And what about the accidental property investor, or - for example couples who buy a home together while still keeping properties they owned before they met, or those who have inherited property? How many of these are aware of those 22 changes to the tax regime? For all property investors, not just the accidental ones, it could be time to speak to an expert to help unravel the myths attached to property investment once and for all.