The page you were trying to view is not available for your role and region.

Bed and ISA – the practice of selling investments held outside an ISA and then buying them back under the ISA tax wrapper – is a familiar concept, but for high-net-worth individuals, Bed and Pension can make more sense. The essence of either of these moves is to increase the tax efficiency on existing investments and recent changes to tax allowances have added to the attraction of moving investments into a SIPP (self-invested personal pension), a process known as Bed and Pension.

The reduction in capital gains tax (CGT) allowance - from £12,300 in the 2022/23 tax year to only £3,000 from April 2024 onwards – has increased the tax burden on investments held outside of tax wrappers. Bed and ISAs are one of the most popular solutions to improve tax efficiency and shield investment gains from HMRC, but for those with sizable investment portfolios the £20,000 annual limit is restrictive.

Increased pension allowance

In contrast, the 2023/24 tax year saw the pension allowance increase to £60,000. And unlike the ISA allowance, unused pension allowances from the preceding three years can be utilised.

Moving taxable investments into a pension can, under the right circumstances, increase long-term tax efficiency for investment returns, whilst also attracting tax relief on the contributions at the individual’s highest rate.

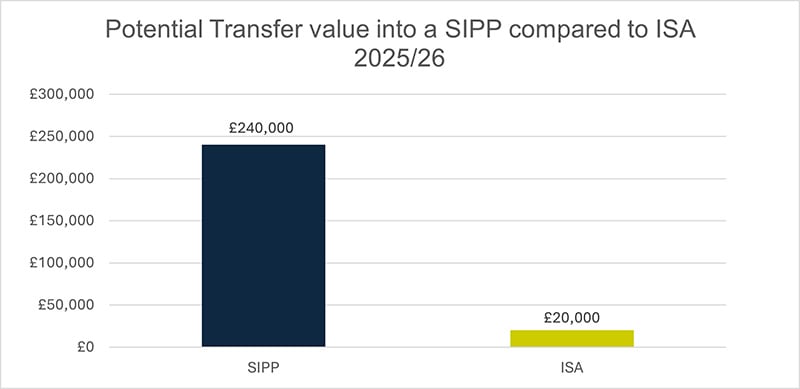

The potential savings into a pension can vary depending on the annual allowance, carry forward, earnings and tapering of the allowance, but at the maximum amount available, an individual utilising the past three years of pension allowance could benefit quite substantially. If a pension exists, but has received no contributions from the individual, this will allow £60,000 for the current tax year, plus £60,000 for each of the preceding three tax years, allowing a potential £240,000 to be moved into the pension in one year, compared to the £20,000 allowable into an ISA.

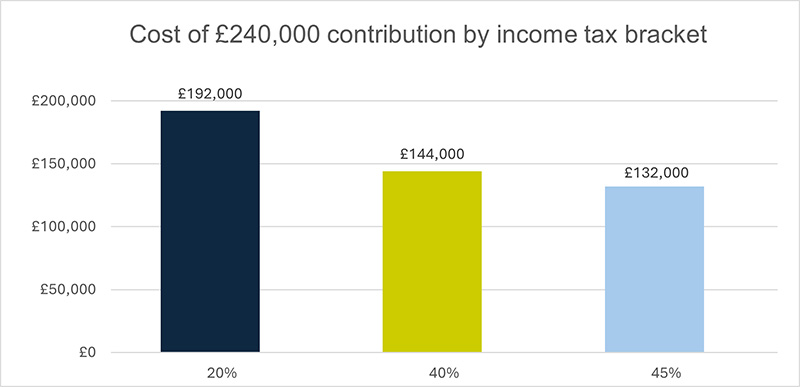

For a joint couple with similar circumstances, £480,000 could be moved into a SIPP in the current tax year, compared to £40,000 in an ISA – that’s 12 times as much! The additional benefit of tax relief being applied to pension contributions at the investor’s highest marginal income tax rate also means a £240,000 pension contribution would only cost a basic rate taxpayer (20%) £192,000. The cost to an additional rate taxpayer (45%) would be further reduced to just £132,000.

It should be noted that you cannot usually access money in a SIPP until the age of 55 (57 from 2028) whereas ISA withdrawals are allowed at any time, while the personal tax treatment depends on individual circumstances and may change in the future. However, for a high-net-worth individual with little expected need for the money in the near-term future, the tax benefits of Bed and Pension can outweigh those on offer in an ISA, depending, of course, on the investor’s objectives, income and access needs.

Quilter Cheviot

Senator House 85 Queen Victoria Street London EC4V 4AB +44 (0)207 150 4000

enquiries@quiltercheviot.com

quiltercheviot.com

This is a marketing communication.

Investments and the income from them can go down as well as up, you may not get back what you invest.

This material is not tax, legal or accounting advice and should not be relied on for tax, legal or accounting purposes. Quilter Cheviot does not provide tax, legal or accounting advice. You should consult your own tax, legal and accounting adviser(s) before engaging in any transaction.

Quilter Cheviot and Quilter Cheviot Investment Management are trading names of Quilter Cheviot Limited and Quilter Cheviot International Limited. Quilter Cheviot International is a trading name of Quilter Cheviot International Limited.

Quilter Cheviot Limited is registered in England and Wales with number 01923571, registered office at Senator House, 85 Queen Victoria Street, London, EC4V 4AB. Quilter Cheviot Limited is a member of the London Stock Exchange and authorised and regulated by the UK Financial Conduct Authority and as an approved Financial Services Provider by the Financial Sector Conduct Authority in South Africa.

Quilter Cheviot International Limited is registered in Jersey with number 128676, registered office at 3rd Floor, Windward House, La Route de la Liberation, St Helier, JE1 1QJ, Jersey and is regulated by the Jersey Financial Services Commission and as an approved Financial Services Provider by the Financial Sector Conduct Authority in South Africa.