The page you were trying to view is not available for your role and region.

The government offers generous tax incentives for taxpayers contributing to pensions, in an effort to encourage individuals to save for retirement.

Broadly, the current system offers three key ‘carrots’ to incentivise saving:

- Income tax relief for individuals making pension contributions (up until age 75), and tax incentives for firms contributing – in addition, firms must contribute a minimum to most employees’ pensions via auto-enrolment

- Investments in a pension grow free of income tax and capital gains tax

- Up to 25% of the pot* can be taken tax free, upon retirement. The remainder is subject to income tax at an individual’s marginal rate, but no National Insurance

*Subject to the available Lifetime Allowance

Here, we are going to focus purely on the first aspect - tax relief on individual contributions (relief on company contributions is granted via a different mechanism).

You should also note that this guidance is aimed at taxpayers in England and Wales; whilst the mechanics are the same in Scotland, there are different tax rates in force.

I’ve found this is an area that regularly leaves clients confused, which is completely understandable given the mechanics of how tax relief is granted!

So, let’s start with the basic concept. In a single tax year, if you pay a contribution into a pension you are entitled to income tax relief at your marginal tax rate, up to the maximum of your Relevant UK Earnings (broadly salary or self-employed earnings, but not dividends or rental). There are limits you need to bear in mind, which I’ll cover later, but this means:

- Non-taxpayers: even those who do not earn enough to pay income tax are entitled to income tax relief at the basic rate, meaning £100 in a pension costs just £80 of take home pay, provided it’s paid via ‘relief at source’ which I’ll cover later. Furthermore, even those who have no earnings can contribute up to £2,880 net (£3,600 gross), so they could physically pay £2,880 to a pension and benefit from tax relief of £720 (claimed by the scheme from HMRC), taking the value in the pension to £3,600.

- Basic rate: the basic rate of income tax is 20%, so basic rate taxpayers are entitled to 20% tax relief. Again £80 of take-home pay means £100 goes into a pension

- Higher rate: the higher rate of income tax is set at 40%, so £100 in a pension comes from giving up £60 of take-home pay, the effective cost to you

- Additional rate: the additional rate of income tax is currently 45%, meaning £100 in a pension should cost just £55.

So, the aim of these measures is that your contributions should result in you effectively avoiding the income tax you would have paid on the highest level of earnings. However, to benefit fully from this system many higher and additional rate taxpayers need to do some additional legwork!

Some things to bear in mind:

Whilst the highest published rate of income tax is 45%, I should also mention that there are two ‘tax traps’ which mean individuals can end up paying an effective rate of 60% on certain earnings. The first are higher rate taxpayers impacted by the ‘High Income Child Benefit Charge’ whereby those receiving child benefit and earning over £50,000 lose child benefit at a rate of 1% for every £100 of income between £50,000 and £60,000 (the child benefit is entirely lost at £60,000).

The second is for those earning more than £100,000, who begin to lose their personal allowance (the amount you can earn before you pay tax), at a rate of £1 for every £2 of earnings above £100,000, meaning the personal allowance is entirely removed for those earning over £125,140.

In both of these cases, pension contributions can potentially be even more cost effective, saving you from these tax traps. This is a complex area, and you should speak to a financial planner to see what the impact would be in your personal circumstances.

In addition, it’s important to point out that whilst any contribution within your Relevant UK Earnings is eligible for tax relief, there is a limit (called the Annual Allowance) above which an additional tax charge is levied – wiping out the benefits of any income tax relief. The Annual Allowance is £40,000 for most people but can be reduced to as little as £4,000 for very high earners (those on £200,000 or more) or for people who have taken benefits flexible from their pension, such as taking a taxable income via Flexi Access Drawdown. People may be able to avoid an Annual Allowance tax charge by using a provision called Carry Forward (using unused pension allowances from previous tax years), however the intricacies of the Annual Allowance & Carry Forward are complex, and beyond the scope of this article.

Methods of collection pension contributions can differ

There are three methods that are commonly used to facilitate pension contributions in the UK.

If your contributions are collected via net pay or salary sacrifice you will already be receiving the benefit of any higher or additional rate income tax you are due, but I will go through all three as you may not be aware of how your contributions are being paid.

- Relief at Source: A very common method, used extensively for many workplace pensions as well as pensions you may have set up yourself. Essentially the ‘net’ pension contribution is taken after any income has been subject to income tax and national insurance. The net contribution is added to the pension, and the pension provider automatically claims basic rate tax relief on your behalf at your marginal tax rate, EG 20%. This means that if you pay £80 the pension provider will reclaim £20 from HMRC, leaving you with £100 in a pension.

- Net Pay: Taken from pre-tax pay, so no tax relief is due because income tax was not levied on the contribution.

- Salary Sacrifice / Salary Exchange: Similar in many respects to the Net Pay method but differs in that there is an agreement between you and your employer, in which you give up or ‘sacrifice’ part of your salary in exchange for them making a contribution to your pension. In these circumstances, the contribution is treated as coming from your employer. Because the salary you receive is less, you also do not pay Income Tax or National Insurance on that amount, and neither does your employer. This means you will get maximum benefit, and some employers will even pass on their own tax saving to boost the contribution further.

If you are part of a workplace pension, you may be able to get an indication of the collection method by looking at your payslip, which tends to be split into ‘left’ and ‘right’ sides, with the left side showing total gross pay (before tax) and the right side showing all deductions after tax. If your pension is being deducted on the left side, it’s before tax, so will be via Net Pay or Salary Sacrifice, and if from the right side, its likely via Relief at Source.

To tell for certain you can speak to your company’s HR department or check the scheme rules/speak to your provider.

How do you reclaim extra tax relief you may be owed from HMRC?

If you are a higher or additional rate taxpayer, and your pension contributions are being collected via the Relief at Source method, you will need to claim back the tax relief you are due.

Before you can make a claim, you will need to calculate what your gross contributions are and provide this figure to HMRC. You can either do this by asking your pension provider to confirm your gross pension contributions for the tax year in question, or you can calculate them yourself. Because the gross contribution includes the addition of basic rate income tax relief (claimed on your behalf by the provider), you will need to take the net contribution (which is the amount you physically paid) and then divide that by 0.8, to determine the gross figure.

As an example, if you paid a single contribution in the last tax year of £10,000 net (the amount you physically paid) via Relief at Source, you divide this by 0.8, and your gross pension contribution would be £12,500. This is the amount you’ll need to provide to HMRC.

Bear in mind, you cannot claim any additional rate tax relief if any of the following are true:

- You are a non-taxpayer or a basic rate taxpayer

- Your contributions are collected via net pay or salary sacrifice

- You cannot claim tax relief on the element of contributions paid directly by your employer – only on individual contributions

If you pay contributions to a scheme where basic rate tax relief is not claimed via your provider, and the payments are not an employer contribution, salary sacrifice, or net pay, you need to follow a different process to the one outlined below. This is unusual and is generally the case for either members of a Retirement Annuity Contract or SSASs (Small Self Administered Schemes).

Once you have the gross figure, you can make a claim in the following ways:

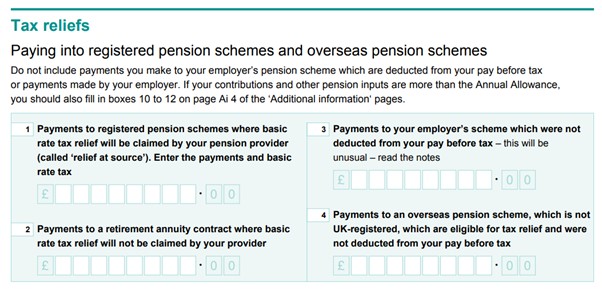

- If you complete a tax return, you can add the gross figure to this. If you are completing a paper return you can add this to box 1 below, and there are the same options via the online return:

- If you do not complete tax returns you can contact HMRC in writing or via telephone, and tell them what your gross pension contributions were in the year in question, you can find HMRC’s contact details here: Income Tax: general enquiries - GOV.UK (www.gov.uk)

I often come across clients in this situation who have not claimed the income tax they are due for several years, so you could be owed money from previous tax years. Generally, the additional tax relief you are owed will either by paid via an adjustment in your tax code (reducing the tax you pay) or via a direct payment, normally a cheque, from HMRC.

Hopefully this guidance is of use to you, however this is a complex area. If you are still unsure after reading this, I would recommend getting in touch with your Financial Planner to talk through how all of this applies to you and your circumstances.

The current pensions system offers very generous tax incentives and being able to make full use of the reliefs available can really help you achieve your retirement goals as efficiently as possible.

Authored by Tom Shorland

Approver Quilter Financial Services Limited & Quilter Mortgage Planning Limited. 28/02/2024