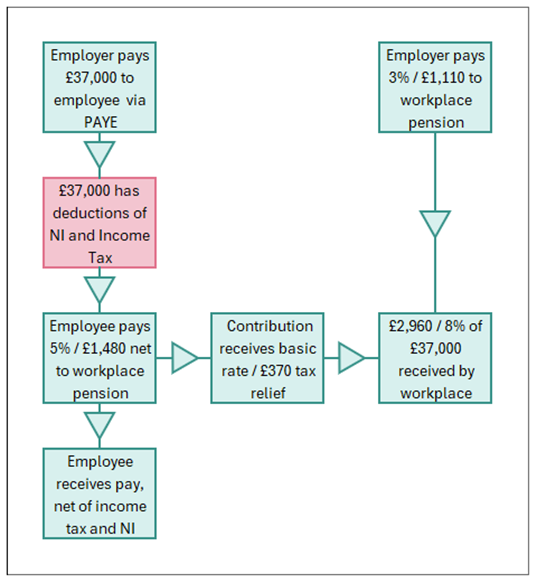

If instead, the employer makes the pension contribution on the employee’s behalf and reduces the employee’s gross salary accordingly, there will no longer be a 5% employee contribution to be assessed. When the pension contribution is handled by the employee, it is subject to National Insurance (NI) through PAYE. However, if the contribution is made by the employer, both employer and employee NI can be saved.

In the current tax year (2024/2025) and next tax year, the savings that would be made by making contributions via this method will be as follows:

|

|

2024 / 2025 Tax Year

|

2025 / 2026 Tax Year

|

|

Employer NI

|

£255.30

|

£277.50

|

|

Employee NI

|

£148.00

|

£148.00

|

Scaling this up to our workforce of 50 employees, all earning £37,000 per annum, the total employer savings would be as follows:

|

|

2024 / 2025 Tax Year

|

2025 / 2026 Tax Year

|

|

Employer NI

|

£12,765.00

|

£13,875.00

|

We covered how this same workforce would be costing their employer an additional £52,500 from April 2025. By changing to this alternative pension contribution method, £13,875 of that could be offset and any saving made will be on an annual basis.

This alternative method of contribution to a workplace pension is known as salary sacrifice, or salary exchange.

Key Points to Consider

It is important to understand that our example uses a uniform workforce, all earning the same amount. In practice, employees will earn different amounts and will have different circumstances.

In the current tax year, the national minimum wage is set at £11.44 per hour or £20,821 per annum based on a 35-hour working week2. This is increasing to £12.21 (£22,222 per annum) from April 2025. It is important that salary sacrifice is not implemented for employees whose effective hourly rate would be brought below the minimum wage by salary sacrifice.

Part time staff may also earn at an effective rate well over the minimum wage, but if their earnings are not at a level that results in employee national insurance being due (based on hours worked or pro-rating), salary sacrifice is not likely to be suitable.

These are important considerations that should be addressed by a knowledgeable professional who is able to properly assess a company’s workforce and identify possible pitfalls.

If you have further interest in exploring whether these savings are available to your company, it is worth discussing them with either a corporate financial adviser or an accountant specialising in employee benefits.

Tax treatment varies according to individual circumstances and is subject to change.

Tax Planning is not regulated by the Financial Conduct Authority.

Sources

1 Office for National Statistics. Employee Earnings in the UK: January 2025. Office for National Statistics. [Online] January 2025. Based on median gross annual earnings in April 2024 - £37,430 per annum. Employee earnings in the UK - Office for National Statistics

2 Department for Business and Trade. Working Hours for which the minimum wage must be paid. Gov.uk. [Online] January 2025. Note that while 35 hours is a contractual standard, it is the hours actually worked by employees that determines what an annual equivalent salary would be.